What happens when thousands of New Yorkers rush to list their homes just as buyers hit their seasonal slowdown? That’s the paradox of Manhattan real estate every September—a flood of fresh inventory meets a dip in signed contracts. It looks chaotic from the outside, but with the right perspective, it’s actually the rhythm of the market.

Why September Feels Different in NYC Real Estate

If you’ve been around the New York market for more than a minute, you know fall is the “other” busy season. Spring gets all the attention, but September is when the lights come back on after summer. Families return from the Hamptons, Wall Street is back from vacation, and suddenly everyone remembers they were supposed to be looking for an apartment.

But here’s the tricky part: supply and demand don’t move in lockstep. New listings surge in September, while demand—measured by contracts signed—usually bottoms out before picking back up in October and November. That overlap creates an odd moment where it feels like the market is flooded, but deals are slow to materialize.

Supply Picture: Tight, But Moving

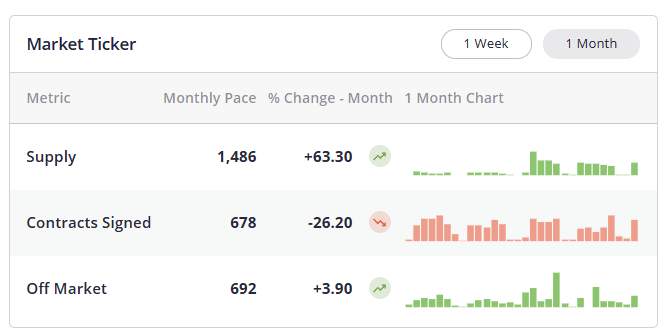

As of mid-September 2025, Manhattan supply sits around 1,486 active listings. By seasonal standards, we’d normally see about 1,757 by month’s end. So yes, inventory is climbing, but it’s still lean compared to historical norms.

For buyers, this means a bit more choice than the summer doldrums, but not the kind of glut you might read about in national housing headlines. For sellers, it’s a reminder that “competition” is relative. A well-priced, well-presented listing can still stand out quickly.

Buyer Demand: Seasonal Bottoming

Contracts signed over the past 30 days clocked in at 678, just shy of the 707 average for September. That sounds like a shortfall, but it’s actually part of the pattern: September is the bottom for deal activity, while October and November are when contracts really pop.

Think of it this way—September is the setup; October is the payoff. Sellers get their homes in front of buyers now so that when demand accelerates, they’re already in the mix.

Macro Winds Blowing Through Manhattan

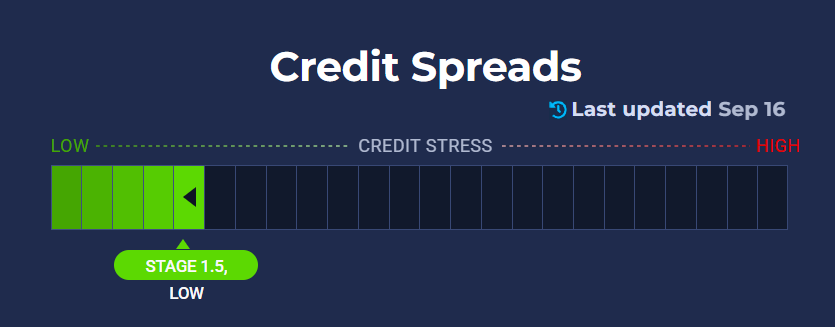

You might wonder why we’re talking about credit spreads and Fed futures when this is supposed to be a housing update. Here’s the thing: Wall Street sentiment has a funny way of trickling down to Park Avenue co-ops.

Right now, credit spreads are low, which signals “risk on.” Translation: financial markets aren’t flashing warning lights. At the same time, the Fed is expected to cut rates three times this year—September, October, and December. Mortgage rates have already responded, drifting lower over the past few months.

But remember, the Fed only controls short-term rates. Long-term rates, which shape 30-year mortgages, depend on bond markets. That’s why sometimes you’ll see the Fed cut and mortgages actually tick higher. The message buyers should hear? Watch the trend, not the headline.

https://www.creditspreadalert.com/

National Signals vs. NYC Reality

Across the country, building permits are down and inventory is piling up. In markets like Austin or Miami, buyers can actually afford to be picky. But New York? Whole different ballgame.

A Resi Club map recently showed the Northeast sitting deep in negative inventory territory compared to six years ago. Translation: the supply squeeze is worse here than almost anywhere else. That’s why national headlines about “cooling housing markets” don’t really apply to a condo on Third Avenue.

Luxury vs. Middle Market

For most of 2023 and 2024, the luxury sector carried Manhattan—$10M+ deals seemed unstoppable. That’s shifting. Recent data shows that sales above $10M are down about 52% year-over-year. Meanwhile, the $2–4M segment is up 7.5%, and the $1–2M tier is holding steady.

Why the change? Cash buyers still dominate, but falling mortgage rates could bring financed buyers back into the mix. If that happens, the middle market may become the new engine of activity this fall.

Office Recovery and the City’s Pulse

You can’t talk about NYC housing without mentioning office space. Class A towers are bouncing back as companies pull people into hybrid routines. Class B buildings? Still struggling. But the fact that the top tier is recovering matters, because it signals confidence returning to the city’s core. And confidence has a way of spilling into residential markets.

Timing Your Listing: Why Now Beats November

Here’s where strategy comes in. If you list in late September, you ride the wave of buyers who sign in October and November. Miss that window, and you risk hitting the Thanksgiving slowdown.

Waiting until November means your price cut window falls in December or January—traditionally dead zones. The smarter play is list now, gauge buyer traffic, and if you don’t get an accepted offer in 2–4 weeks, adjust your price while there’s still runway left in the fall season.

What Buyers and Sellers Should Take Away

-

Inventory is rising but still tight.

-

Mortgage rates are trending down, though market sentiment could shift.

-

Luxury is softening while the middle market looks stronger.

-

Seasonal timing is everything—sellers should act now, not later.

-

National housing trends don’t map neatly onto NYC.

The market’s not easy, but it’s not uncharted either. The patterns are there if you know where to look.

A Final Word

Buying or selling in Manhattan this fall isn’t about waiting for perfect timing—it’s about having the right strategy for the season we’re in. If you’re thinking about listing, the next few weeks are critical. And if you’re buying, the softer September demand could give you a window before competition heats up in October.

If clarity and strategy are what you need, let’s talk. Whether it’s prepping your apartment, sharpening your offer, or mapping out the right entry point, I’ll help you move with confidence in a market that rewards preparation.