What happens when fewer sellers list, buyers keep one foot out the door, and the Federal Reserve toys with rate cuts just as New Yorkers return from the Hamptons? You get a real estate market that feels both steady and strange.

Supply Slips, Demand Drifts

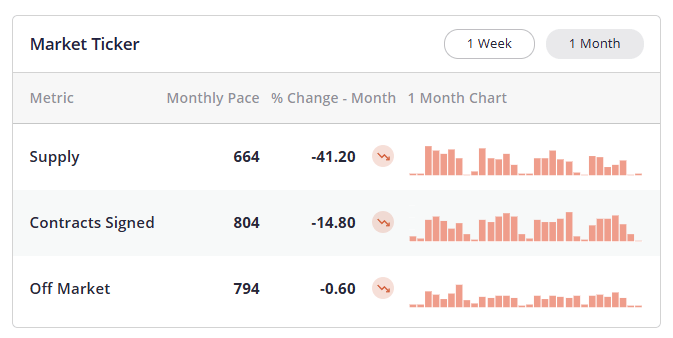

Let’s start with the numbers. Manhattan has logged just 664 new listings over the past 30 days. For late August, the seasonal norm is closer to 943. That’s not a rounding error; that’s a real shortfall.

Contracts signed, meanwhile, came in at 804, when we’d normally expect around 854. Demand is softer than spring, but the bigger story is supply. It’s simply not showing up. That imbalance is what’s nudging the market pulse upward.

And here’s the nuance: rising pulse doesn’t mean buyers are suddenly charging back. It means sellers are getting a relative edge because fewer homes are on the shelf. It’s like walking into a grocery store the week before a snowstorm — even if shoppers are fewer, the half-empty shelves make every gallon of milk feel more valuable.

Credit Spreads, Rates, and the Macro Backdrop

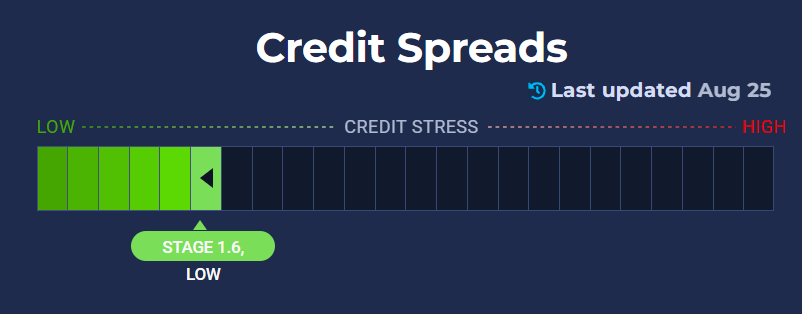

Of course, real estate doesn’t move in isolation. Traders and investors keep one eye on credit spreads — the gap between corporate bond yields and Treasuries — as an early warning sign. Right now, spreads are mostly drifting sideways, a sign of stability. But history tells us that when spreads widen fast, lending slows, stock markets stumble, and mortgages tighten.

Rates are another puzzle piece. The Fed fund futures market is pricing in an 86% chance of a quarter-point rate cut in September, with another possible cut in December. Nothing dramatic, but enough to keep mortgage watchers on edge. Mortgage rates have already slipped a touch in recent weeks, and if jumbo loan pricing keeps undercutting conforming loans, banks may be signaling they’re hungry to lend.

Still, caution is warranted. Inflation isn’t fully tamed, and with equities at record highs, the Fed doesn’t have unlimited room to cut without raising eyebrows. Think of it as trying to steer a crowded subway car — one wrong shift and the balance tips uncomfortably.

https://www.creditspreadalert.com/

A Yield Curve That Won’t Behave

The yield curve — that line connecting short-term and long-term Treasury yields — has been a faithful recession predictor for decades. An inverted curve (short-term yields higher than long-term) usually flashes warning lights. A year ago, inversion was deep. Today, it’s less extreme, edging back toward normal.

That suggests the economy may be sturdier than skeptics feared. But yield curves can whisper before they shout. Just because a recession didn’t arrive on cue doesn’t mean risks disappeared. Still, for housing, the slow “de-inversion” is at least a hint that the backdrop is healing rather than unraveling.

https://www.investing.com/rates-bonds/usa-government-bonds

National Housing Softness vs. Manhattan Stubbornness

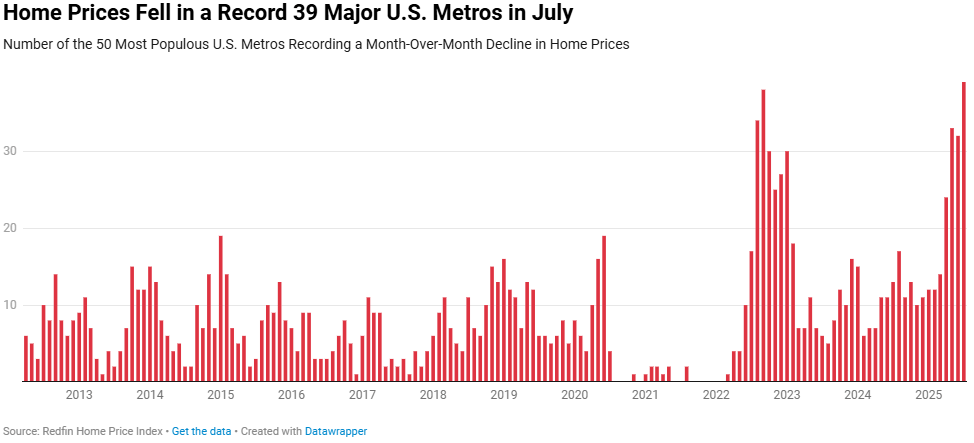

Zooming out, 39 of the nation’s 50 largest metro areas are posting month-to-month price declines. Builders have pulled back, too. Single-family housing starts are down across most regions, with Southern California off 33% and Florida down 22%. Only parts of the Midwest are showing a surprise uptick.

Manhattan, though, marches to its own beat. Prices here haven’t spiked the way they did in Sunbelt markets, so the comedown is less severe. Instead, we’re watching a sideways shuffle: fewer deals, fewer listings, and prices that won’t budge unless a seller gets serious with a cut.

And that’s the paradox — rents remain high, mortgage costs still strain buyers, but the lack of supply props up values. It’s less boom or bust, more a stalemate.

https://x.com/charliebilello/status/1957781109472706564/photo/1

The Seasonal Playbook: Fall Is Short, Sharp, and Strategic

Here’s where local rhythm matters. September is Manhattan’s biggest listing month, but it’s a compressed season. Most inventory hits mid-September. Buyers truly engage in October. If a listing isn’t in contract by mid-October, the clock is already ticking toward a price cut.

By November, attention shifts — first to turkeys, then to travel. December brings the occasional buyer who made a year-end promise to themselves, but the data shows slim odds. The smarter move is to treat fall as a sprint, not a marathon.

What Buyers and Sellers Should Watch

-

For buyers: Don’t mistake a rising market pulse for heated demand. It’s about thin supply. If the right place appears, be ready, but don’t expect a stampede of competition below $4M.

-

For sellers: Time your pricing with precision. If you’re not getting traction by mid-October, adjust before the market goes into holiday hibernation.

-

For agents: Context is everything. Explaining why pulse is up, even while contracts lag, is key to guiding clients through the noise.

Closing Thoughts

Manhattan’s real estate market, late summer 2025, is a puzzle of contradictions. Supply is lighter than expected, demand has cooled, yet sellers aren’t without leverage. Credit spreads and yields whisper stability, even as national housing weakens. And the fall season, short as it is, could tell us whether this market is quietly resetting or simply catching its breath.