Supply’s easing, contracts are holding, and the Fed’s next move has everyone guessing. Here’s what’s really happening as Manhattan heads into the final stretch of the year.

Is Manhattan’s market quietly gaining traction—or just catching its breath before the holidays?

November has always been an odd month in New York real estate. The weather turns, the marathon passes, and brokers start talking about “the last good weeks” before Thanksgiving distractions set in. But this year? Something feels different. The usual late-fall lull isn’t as quiet as it looks on paper—and that’s what’s catching smart agents’ attention.

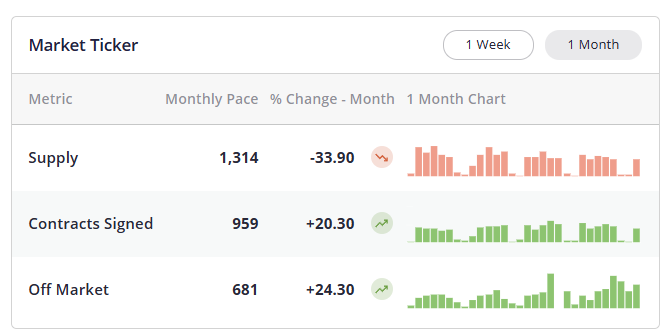

Supply Is Sliding, but Contracts Are Holding

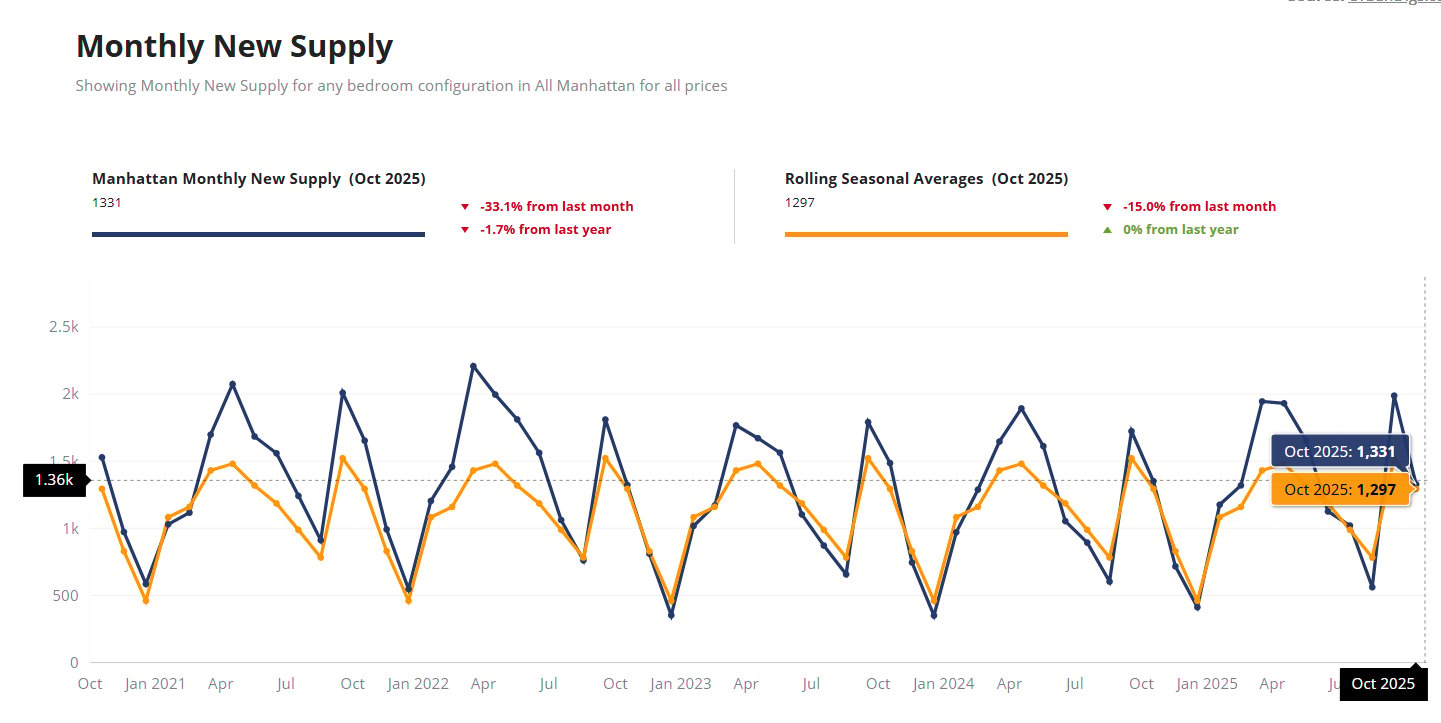

Let’s start with the numbers. Manhattan’s 30-day new supply just clocked in around 1,314 listings, well below last year’s level and set to dip under 1,000 by the end of November. That’s a meaningful shortfall for this time of year.

On the demand side, contracts signed sit near 959—a strong number for late fall and well above seasonal expectations. UrbanDigs’ “Market Pulse” (the ratio of contracts to active listings) has nudged upward for the second straight month, signaling a subtle improvement in listing conditions. The Climate Index—which measures how easy or difficult it is for sellers to find success—also ticked slightly higher, marking steady progress since summer.

Translation: fewer homes are coming to market, but the ones that do are getting traction.

It’s not a rally. It’s a recalibration.

Two Months of Green: What That Actually Means

Here’s the overlooked headline: Manhattan has now logged two consecutive months of above-average deal activity—the first time that’s happened since 2022.

That may sound like a small thing, but in a city where psychology drives as much as pricing, it’s big. It means buyers haven’t retreated, even with higher borrowing costs. It means sellers who priced realistically this fall found takers. And it means that, beneath the quiet surface of November, the market is still very much alive.

Agents on the ground are feeling it too. Open houses are busier, inquiries are up, and even the marathon weekend slowdown didn’t fully stall momentum. One broker joked that “the market’s jogging, not sprinting—but at least it’s moving in the right direction.”

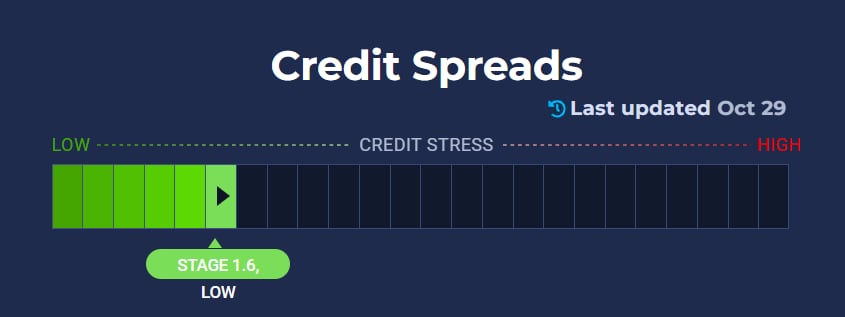

Credit Spreads, Confidence, and Calm Markets

Zooming out for a second—because Manhattan never moves in isolation—the broader financial backdrop is unusually calm.

Credit spreads, the gap between corporate and Treasury yields (think of it as Wall Street’s stress barometer), remain tight. When spreads widen, risk rises. When they stay narrow—as they are now—it signals confidence. “The canary’s still singing”.

Volatility is down too. The VIX (which tracks stock market swings) and the MOVE index (bond volatility) both sit at their lowest levels since 2023. Together, they suggest investors aren’t bracing for chaos.

Why does that matter for housing? Because stability fuels real estate confidence. When investors feel safe taking risk, they keep capital flowing into property markets. And for Manhattan, where so much wealth is tied to Wall Street, low volatility often translates into steadier demand—even when rates are higher than we’d like.

https://www.creditspreadalert.com/

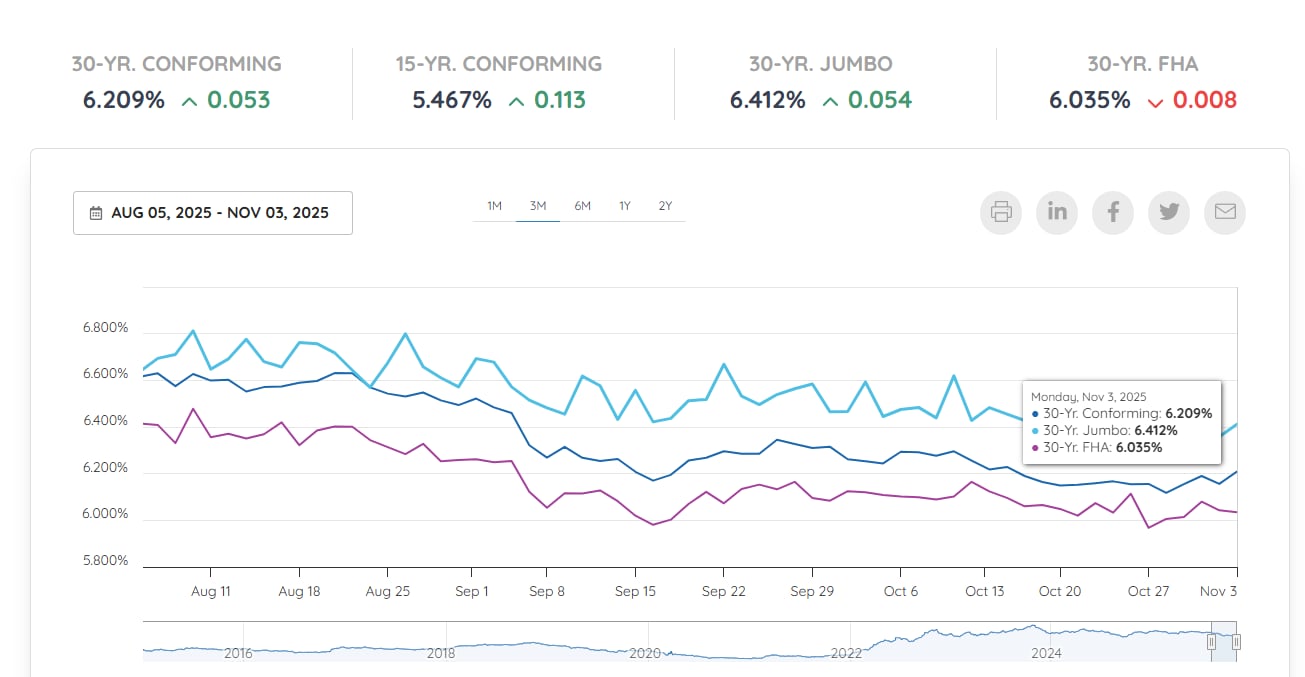

Rates: Sideways, for Now

Let’s talk about those rates. The Fed already delivered its first cut this fall, and futures markets show about a 70% chance of another quarter-point cut in December. But before you start celebrating, here’s the catch: mortgage rates haven’t really budged.

In fact, the average 30-year fixed sits slightly above where it was before the last cut—around 6.2% to 6.3%. That’s because mortgage pricing reacts to long-term bond yields, not directly to the Fed’s short-term rate. Until the spread between the 10-year Treasury and mortgage rates narrows, don’t expect major relief.

Still, the bigger picture is positive. The rate ceiling seems to have passed. We’re not going back to 2022’s double peaks. And sideways is far better than spiking.

https://www2.optimalblue.com/obmmi

Jobs, Banks, and the Underlying Economy

One reason the Fed’s playing cautious? Mixed economic signals.

Job growth remains decent, but cracks are forming in regional banks and consumer-facing sectors like restaurants and retail. Layoffs are inching up, though nowhere near crisis levels. For Manhattan, where much of the buyer base skews professional or investment-driven, these national ripples matter less—but they shape sentiment.

If job softness deepens, the Fed could pause its cuts. And that means mortgage relief might stretch further into 2026.

But for now, the takeaway is stability: not booming, not breaking.

https://x.com/Mayhem4Markets/status/1985348411197968400

National Softness, Local Strength

Nationally, housing looks wobbly. Builders are pulling back, permits are down, and inventory is stacking up in places like Texas and Florida. Prices in some Sunbelt metros are already rolling over.

Meanwhile, Manhattan’s inventory remains near its lowest level since 2019, and Brooklyn’s is only modestly higher year-over-year. That tightness is quietly insulating the city from the kind of corrections showing up elsewhere.

In short: New York isn’t booming, but it’s holding. When other markets sneeze, Manhattan tends to sniff—but rarely catches the full cold.

Seasonality: The Final Window of 2025

November is the market’s twilight season. By the week of Thanksgiving, attention shifts—first to turkey, then to travel, then to holiday lights.

If your listing isn’t in contract by mid-November, chances are slim you’ll close before year’s end. For sellers, that means one thing: act now or price strategically for a January relaunch. The worst move is waiting until December to make adjustments when the audience has vanished.

For buyers, the calculus flips. Fewer active shoppers mean more leverage. Those who stay engaged during this “off” season often secure deals others miss. Think of it as finding value in the quiet—because Manhattan never really sleeps, it just whispers.

The AI Boom, the “Most Hated Rally,” and Why It Matters

One tangent worth noting: the AI investment boom. Tech capital continues pouring into infrastructure—data centers, chip fabs, and software firms—keeping Wall Street exuberant despite muted fundamentals. They called it “the most hated rally in history,” a market everyone distrusts but no one can fight.

That paradox matters. It means risk appetite persists even amid skepticism. For real estate, that translates into steady high-end liquidity, especially in Manhattan’s luxury tier. When the top of the market stays active, it filters confidence down through the midrange.

Resilience Over Hype

So what do we make of this fall’s mixed signals?

-

Supply is shrinking faster than demand.

-

Contracts are outperforming expectations.

-

Volatility is low.

-

Rates are steady.

-

And yet, sentiment still feels cautious.

That combination doesn’t scream “boom,” but it does whisper “resilience.”

After three years of pandemic-era extremes, Manhattan’s returning to something resembling normal—where deals hinge on strategy, presentation, and timing, not panic or FOMO. In a strange way, that’s the healthiest sign of all.

Final Thoughts: Calm Is the New Competitive

The late-2025 Manhattan market isn’t dramatic—it’s disciplined. Two straight months of above-average contracts prove activity hasn’t vanished; it’s just smarter.

Buyers are selective. Sellers are pragmatic. And agents who can articulate nuance—not just headline soundbites—are winning trust.

The market’s quiet hum is easy to miss, but it’s there. Beneath the stillness lies a city that’s learning how to move again—deliberately, confidently, and yes, still very much on its own terms.

Thinking About Your Next Move?

Whether you’re aiming to list before year’s end or planning ahead for 2026, now’s the time to get clear on your strategy.

From understanding the Fed’s next signal to timing your listing before the holiday slowdown, a little foresight can make a big difference.

Reach out today, and let’s map out your next step—so when this quiet market speaks up again, you’re ready to move.