You can feel it—the subtle hum of a market that refuses to play by the rules. Mortgage rates are sliding, stocks are soaring, and yet buyers are still hesitating. Manhattan real estate in October 2025 isn’t chaotic; it’s contemplative. The city’s housing market is balancing delicately between optimism and fatigue, with sellers trimming expectations and buyers scanning headlines for clues.

But if you look closely, this isn’t a market in crisis—it’s a market recalibrating.

A Market That Feels Off-Beat

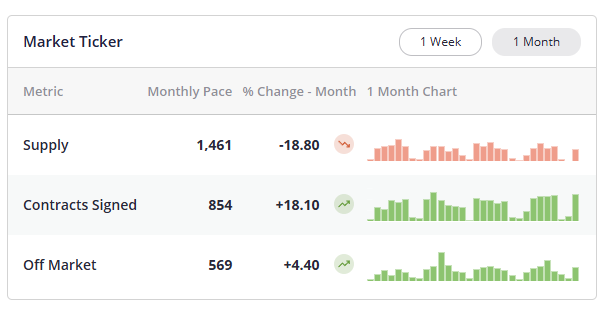

The latest UrbanDigs data says it all. Over the last 30 days, Manhattan saw 1,461 new listings, below the seasonal average of 1,525. Contract activity, meanwhile, came in around 854, up slightly from September but still shy of the 910 benchmark for this time of year.

Translation? Inventory is shrinking faster than deals are closing. That imbalance gives the illusion of strength— a “rising pulse”—but in reality, it’s just math. Fewer listings make the market look tighter, not necessarily stronger.

Think of it as a quiet dance between supply and demand, with neither partner fully leading. September was high, October is soft, and we’re in that classic pre-holiday fade.

Rates and the Fed: Two Cuts, Zero Guarantees

Here’s the headline everyone’s watching: Two rate cuts are priced in. Markets are betting on a quarter-point trim on October 29 and another on December 10.That’s good news, right? Well, sort of.

Mortgage rates have already started to adjust in anticipation. Jumbo loans that hovered above 7% earlier this summer are now around 6.3%, and some relationship banking clients are even landing in the high fives. The catch is that much of this good news is already “baked in.”

When the Fed finally makes its move, mortgage rates may not fall much further—they might even tick up. It’s like buying concert tickets after the headliner’s announced: the excitement’s already priced into the cost.

The broader takeaway? We’re entering a lower-rate environment, but not a cheap one. The age of 3% mortgages is gone. The goal now isn’t chasing rates—it’s leveraging stability.

https://www2.optimalblue.com/obmmi

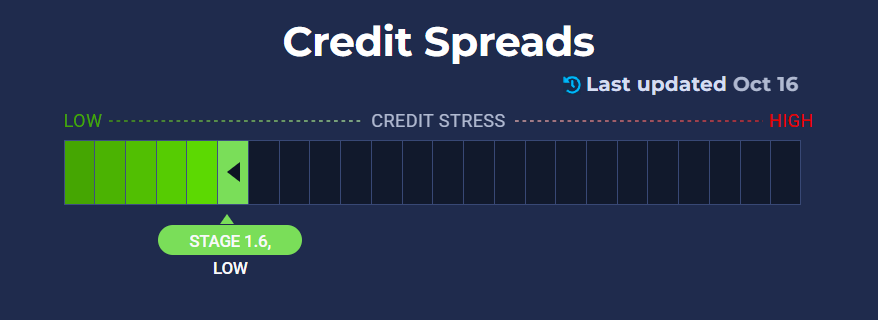

Credit Spreads: The Canary Is Still Singing

Credit spreads (the gap between corporate bond yields and U.S. Treasuries) are the financial world’s early-warning system. When they widen, stress is rising. When they narrow, investors are relaxed.

Right now, they’re relaxed. After a brief jump to Stage 2.1 last month—thanks to tariff headlines—they’ve slipped back into calm territory. That means risk-on sentiment is alive and well on Wall Street.

For real estate, that matters. Stable spreads keep liquidity flowing, lending confidence up, and mortgage volatility down. Until those spreads spike again, the likelihood of a major housing disruption remains low.

https://www.creditspreadalert.com/

Hyperlocal, Not Hyperspeed

Here’s the thing about today’s Manhattan market: broad metrics are nearly useless without context.

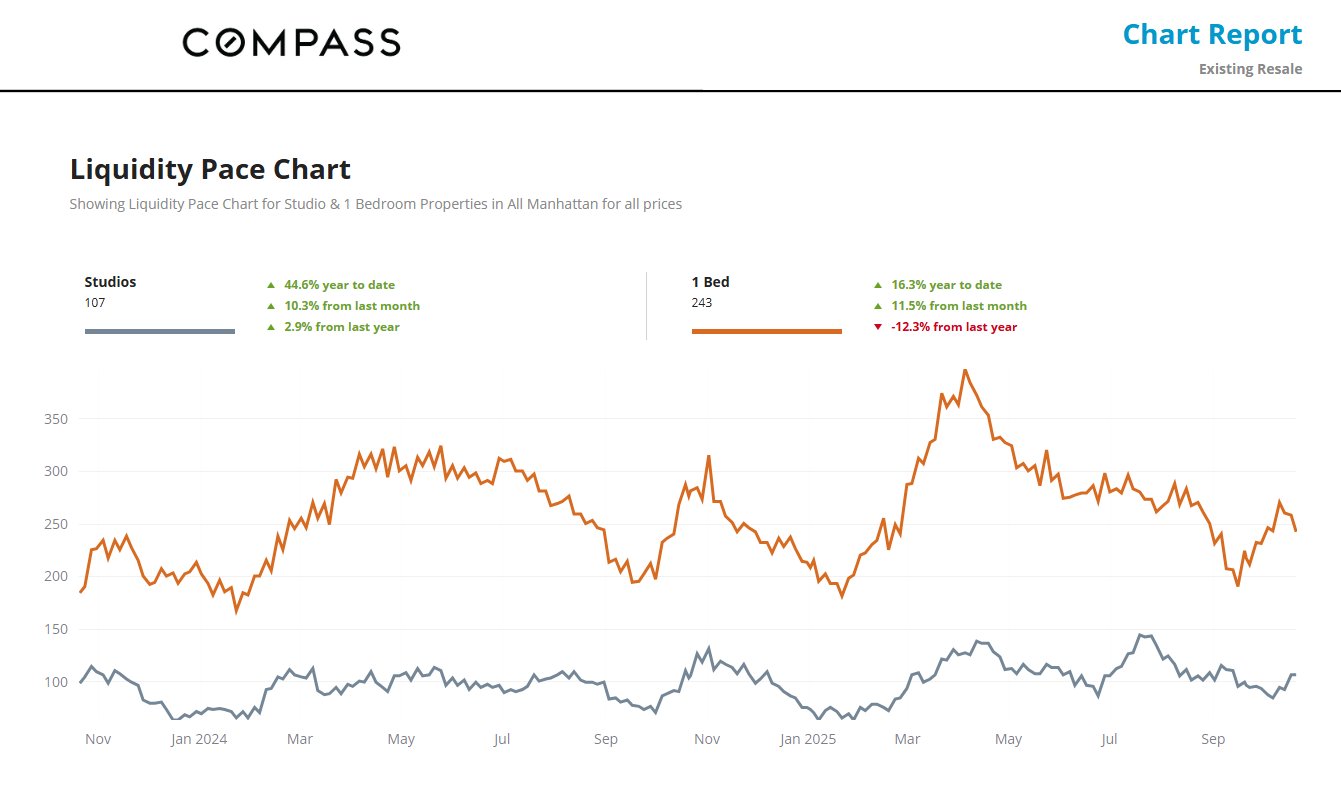

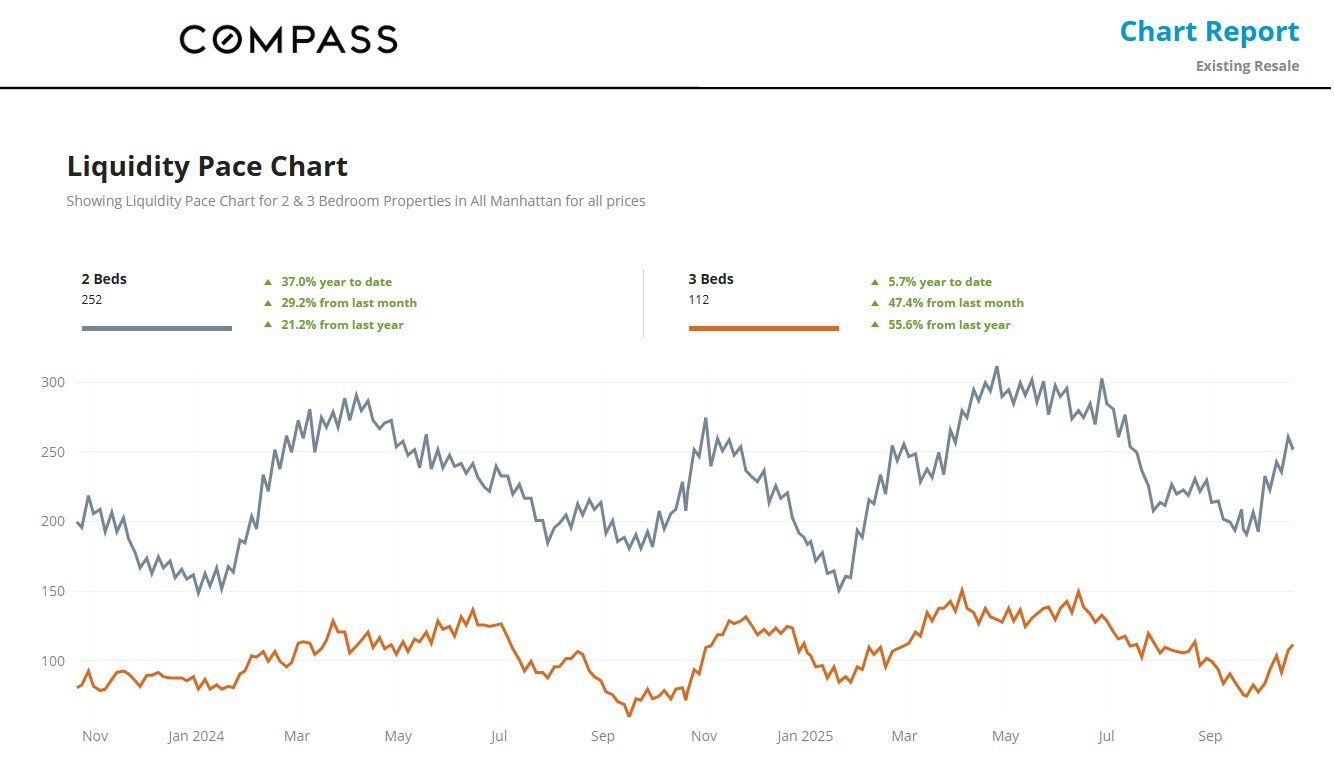

UrbanDigs’ liquidity pace chart shows it clearly—two- and three-bedrooms are outperforming, while studios and one-beds lag. Larger homes with functional layouts are still moving, while compact starter units feel stagnant.

That divide isn’t just data; it’s psychology. Post-pandemic buyers want flexibility—space for hybrid work, for guests, for a quieter life inside the city’s chaos. Smaller units, once prized for efficiency, are suddenly struggling to keep up.

If your one-bedroom has been sitting for 90 days, don’t take it personally. It’s not you; it’s your sector.

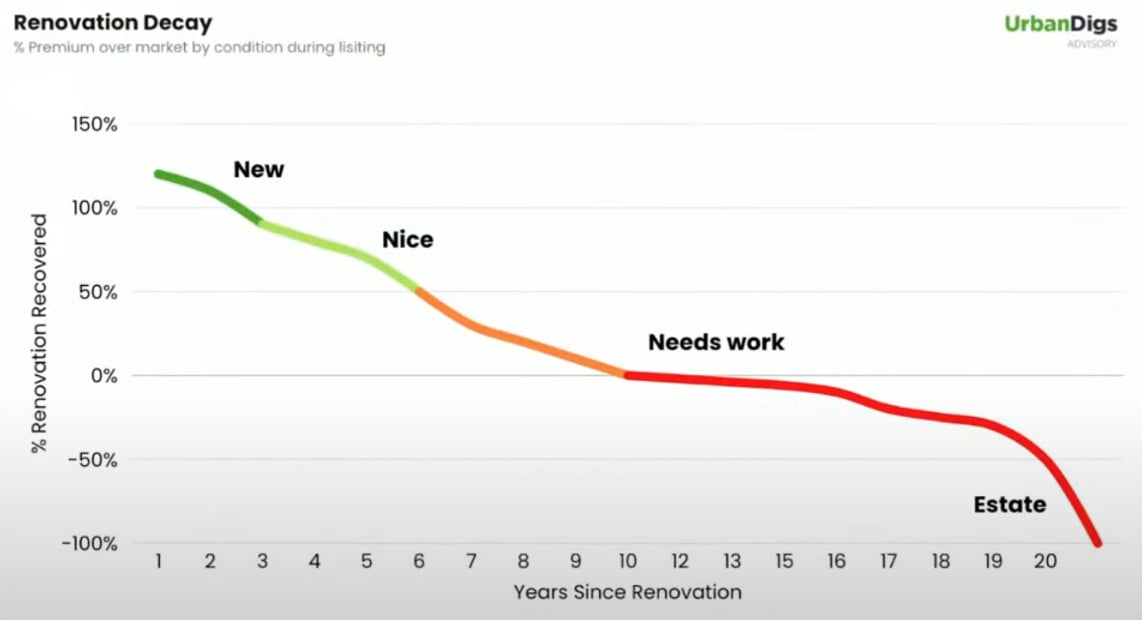

Renovation Decay: The Silent Price Killer

Let’s talk about the elephant in the open house: renovations.

Buyers in 2025 aren’t rewarding “nice.” They’re rewarding “new.” A kitchen redone seven years ago may look timeless to the seller—but to today’s buyer, it’s a $300,000 project waiting to happen.

UrbanDigs calls this “renovation decay.” The market has quietly adjusted its math on what dated finishes are worth. The spread between renovated and unrenovated apartments has tightened from 30% during the pandemic to around 16% today—but the penalty for “used to be nice” has steepened.

And renovation costs? They’ve ballooned. What once cost $300 per square foot now easily crosses $500–$1,000, depending on scope and taste. Labor hasn’t eased, materials have only partially stabilized, and boards are slowly relaxing work restrictions after years of post-pandemic backlog.

For sellers, that means one thing: if your renovation is older than 10 years, price like it’s unrenovated. Buyers aren’t paying for your memories—they’re budgeting for their contractors.

Beyond Manhattan: A National Slowdown

Outside the city, the story’s different. Builders across the country are cutting prices by double digits. In some regions, like Southern California and Florida, new construction prices are down 20–25% from their 2022 peaks.

UrbanDigs data points to what economists are calling a “housing recession” in 30+ states.

But Manhattan? It’s been in its own lane. Prices here never spiked 40% during the pandemic, so there’s less room to fall. That’s why the city’s market looks boring compared to the rest of the country—flat prices, limited supply, and a tug-of-war between patience and urgency.

It’s not boom or bust. It’s equilibrium.

https://x.com/nickgerli1/status/1978495357525897605

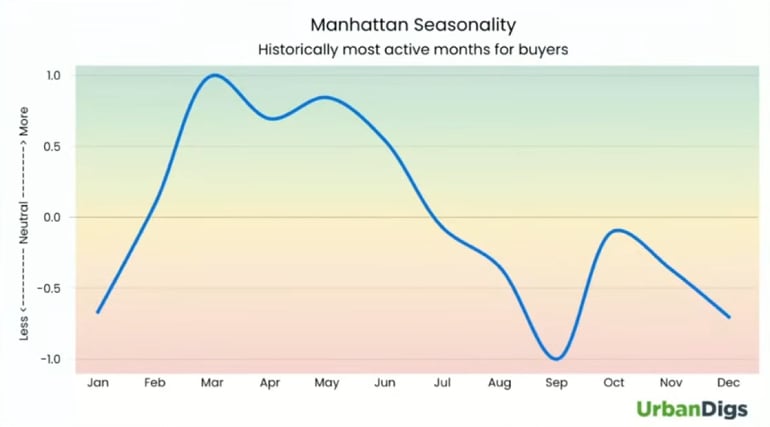

Seasonality: Surfing the Fall Wave

UrbanDigs’ seasonality chart says it best: we’re at the peak of the fall wave. October is the sprint before the slowdown.

By early November, attention shifts from listings to long weekends. By Thanksgiving, the market’s basically in hibernation.

If you’re a seller waiting to cut price after the election or after Thanksgiving, reconsider. Once December hits, buyer energy collapses until spring.

If you’re a buyer, though, this is your sweet spot. The next two weeks could offer the best mix of options and negotiation leverage before inventory resets in 2026.

Election Year Jitters—and Why They Don’t Matter Yet

It’s easy to assume the upcoming NYC elections will sway the market, but historically, they don’t. Rate policy is national. Real estate behavior is local.

Still, elections do shape sentiment. Buyers crave clarity more than good news. Once results are in—whether it’s local policy shifts or national leadership—the fog lifts, confidence rebuilds, and deals pick up again. Expect that in March or April 2026.

The Real Story: Recalibration, Not Recession

When you zoom out, the message is surprisingly steady:

-

Rates are easing but already priced in.

-

Credit spreads are calm.

-

Supply remains lean.

-

Demand is cautious but not collapsing.

-

Renovation reality is reshaping seller expectations.

This isn’t the fireworks market of 2021 or the freeze of 2020—it’s something quieter, more analytical. A thinking person’s market.

Buyers are scrutinizing value. Sellers are recalibrating expectations. And smart agents are reading not just the data, but the psychology behind it.

Because in this market, emotion and economics move at the same pace: slowly.

The Bottom Line

Manhattan’s fall 2025 market isn’t thrilling, but it’s fascinating. Beneath the quiet, meaningful shifts are underway—rate cuts that don’t move the needle, buyers who punish outdated design, and a city that stays stubbornly resilient while much of the country stumbles.

Patience, not panic, is the new power move.

Ready to Read Your Market the Right Way?

Whether you’re pricing a pre-war co-op, scouting a postwar condo, or wondering when to jump back in, don’t navigate the noise alone. I’ll help you decode the signals—from liquidity pace to local pricing—so you can move confidently before the fall wave fades.