It doesn’t feel like a boom—but it doesn’t feel like a bust either. Manhattan’s real estate market is ending 2025 not with fireworks or freefall, but with something far rarer in this city: balance.

The Market Pulse: Above Average, Below the Noise

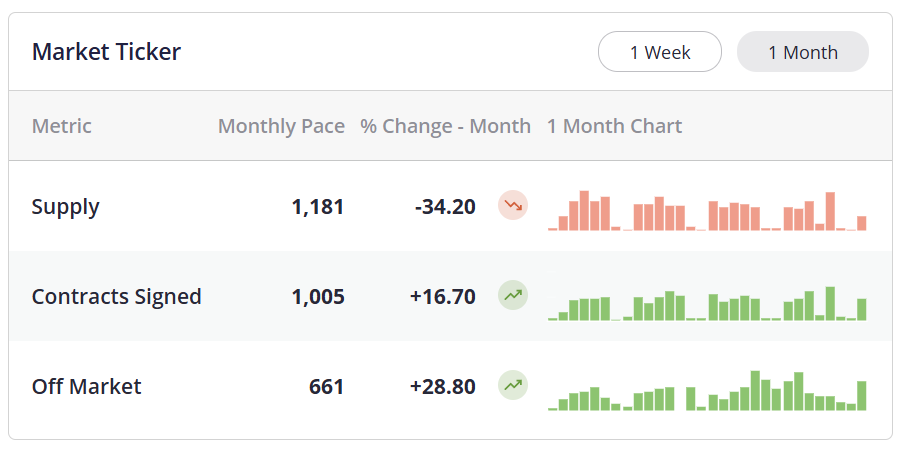

Let’s start with the basics. Manhattan’s 30-day contract activity is running above trend—about 1005 contracts signed this month, compared to the seasonal expectation of 850. That’s not a frenzy, but it’s the strongest streak since 2022, marking the third consecutive month of outperformance.

Supply, meanwhile, is doing the opposite. We entered November with about 1,1181 active listings, well above last month’s totals but trending lower each week. Historically, inventory starts high and finishes low this time of year. That pattern’s playing out again—only this time, the decline feels steeper.

By month’s end, we could dip below the 991 seasonal average, making this one of the leanest late-fall markets on record.

In short: fewer homes, more deals. It’s not euphoria—but it’s quietly bullish.

The Election Effect (Or Lack Thereof)

One of the most surprising takeaways from this month’s UrbanDigs session? The election barely moved the needle.

Despite months of speculation that political uncertainty might stall activity, Manhattan buyers kept signing. The data shows no measurable slowdown in contract volume post-election—proof that NYC’s housing cycle answers more to rates, jobs, and psychology than to politics.

Sure, a different election outcome might’ve shifted confidence or sped up investment. But as it stands, the city’s buyers seem unfazed. They’re focused on lifestyle and long-term value, not headlines.

If anything, this quiet resilience may be one of 2025’s biggest untold stories.

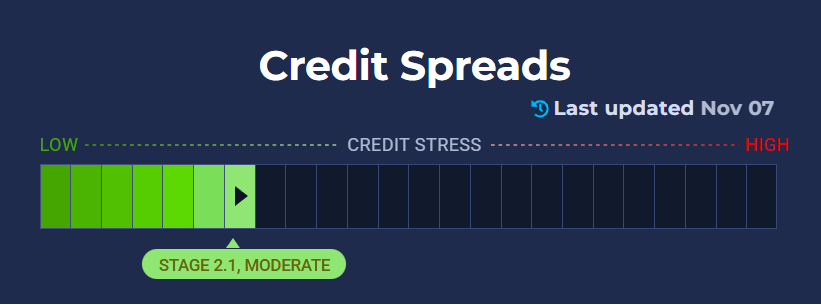

Credit Spreads and the Canary in the Coal Mine

Now, zooming out a layer. UrbanDigs calls credit spreads—the gap between corporate bond yields and Treasuries—the “canary in the coal mine.” When spreads widen, it signals stress: banks tighten, stocks stumble, and borrowing costs climb.

Right now, spreads are hovering near 2.1%, up slightly from last month’s 1.6%. That’s not alarm territory, but it’s worth watching. Two or three consecutive jumps would raise red flags for equities—and eventually, real estate.

Still, context matters. Even at these levels, spreads remain historically narrow, indicating calm credit conditions and steady liquidity. In other words, the financial plumbing is still working fine.

So while headlines elsewhere might scream “slowdown,” the underlying mechanics of risk remain stable. And that stability—paired with light inventory—is keeping Manhattan prices stubbornly firm.

https://www.creditspreadalert.com/

The Fed’s Tightrope: Three Cuts Priced In, Confidence Wobbles

The bond market loves a forecast. Right now, traders are betting on three rate cuts through 2026—one in December, and two more in spring and summer. The catch? Confidence is slipping.

Just a few weeks ago, markets priced a 90% chance of a December cut. That’s now down near 63%, after stronger inflation and jobs data cooled optimism.

That subtle repricing has already nudged mortgage rates higher, even without a single Fed move. The 30-year fixed, which dipped toward the low sixes in October, has crept back up toward 6.5–6.7%, with jumbos still outperforming slightly.

It’s a reminder that the bond market moves between meetings, not during them. Buyers waiting for Powell to wave a magic wand might miss the window—rates are a mood swing, not a milestone.

https://www2.optimalblue.com/obmmi

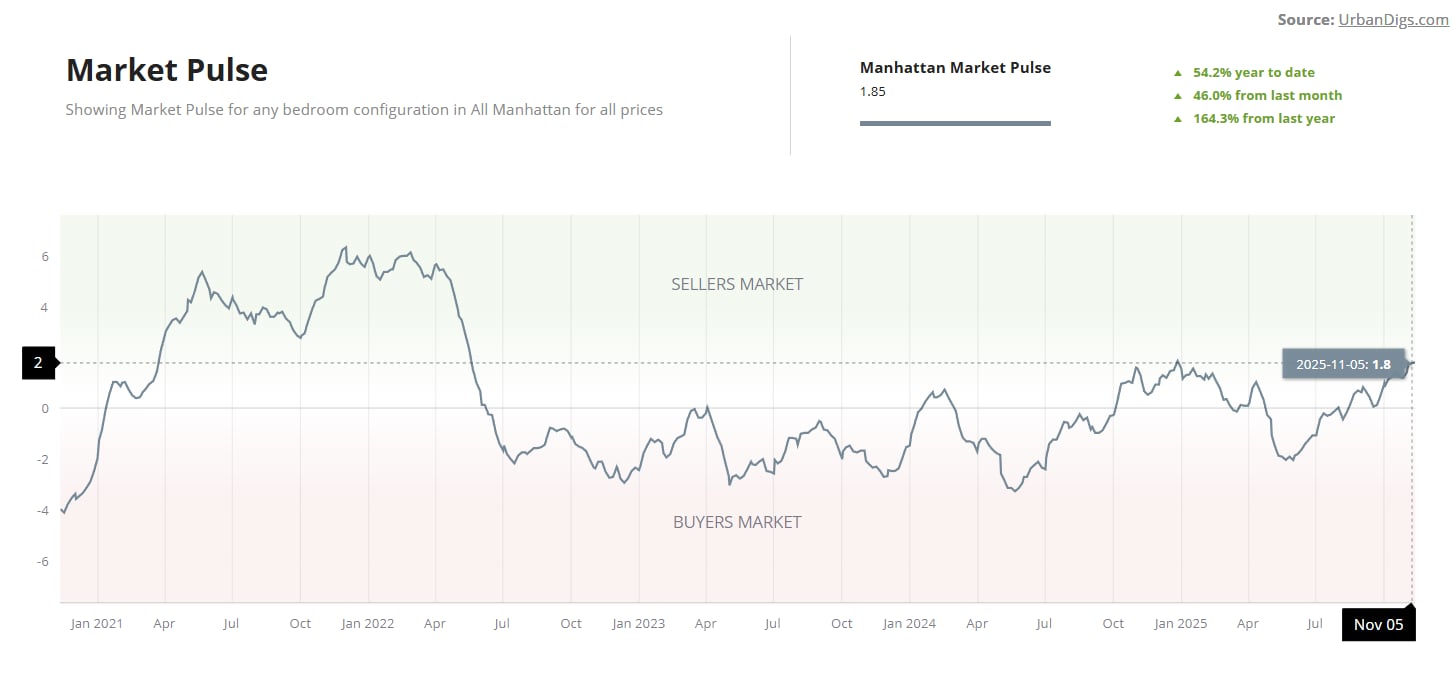

Why Manhattan Feels “Neutral,” Not “Hot”

UrbanDigs’ Market Pulse—a ratio comparing deals to listings—has climbed into what looks like “seller territory.” But don’t be fooled by the chart shading. On closer inspection, Manhattan sits in a neutral-to-seller-biased zone, far from the peak leverage points of 2013–2015 or the pandemic rebound of 2021.

Translation: this isn’t a seller’s market. It’s a steady, negotiated market, where well-priced, well-presented listings move—and the rest linger.

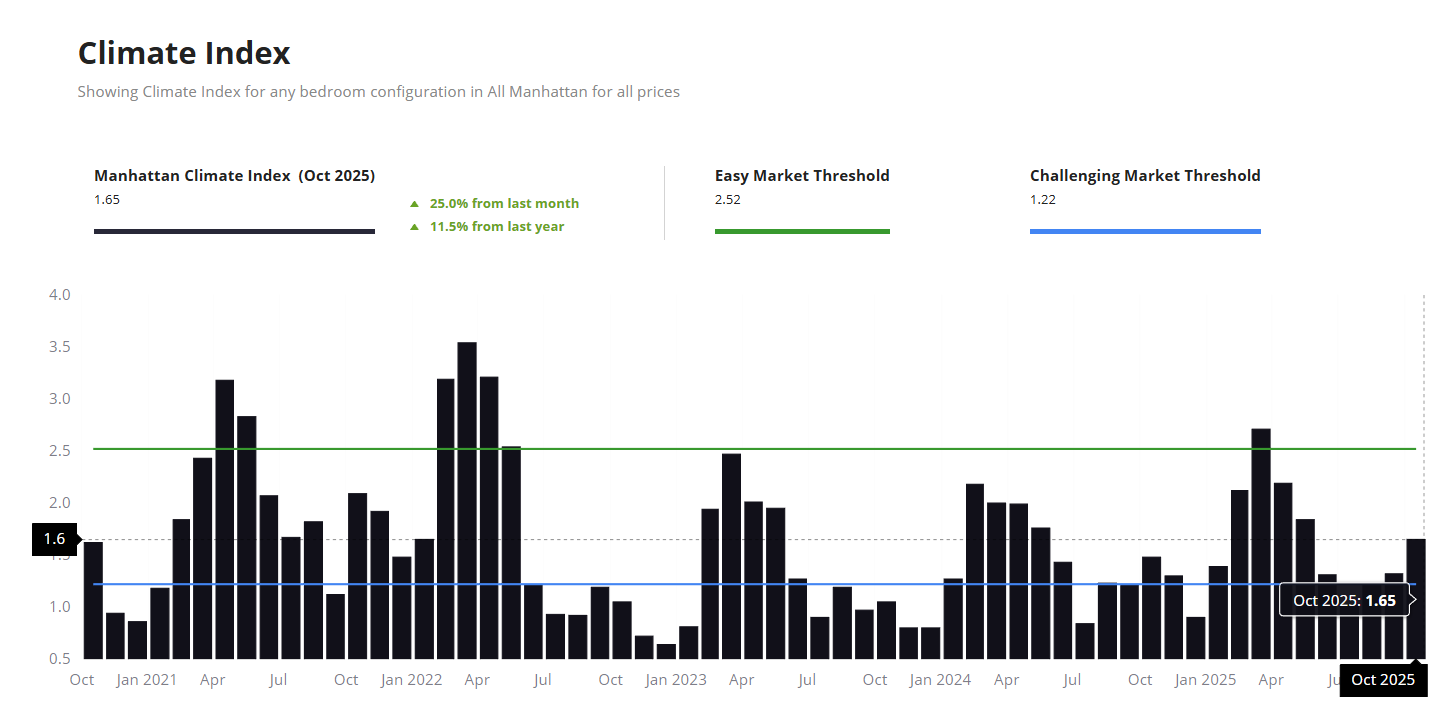

The Climate Index, a measure of how easy it is to sell, backs this up. The bar is closer to “challenging” than “easy,” showing that sellers still need realistic pricing, strong staging, and professional strategy.

In short: the market’s not on fire—but it’s not frozen, either.

The Macro Tug-of-War: Inflation vs. Employment

If you want to understand the Fed’s hesitation, look at the two forces pulling in opposite directions:

-

Inflation: Cooling, but still sticky around 3%, above the Fed’s 2% target.

-

Unemployment: Creeping higher, but slowly.

This tug-of-war is why the central bank’s next move is so hard to predict. Cut too fast, and inflation flares. Wait too long, and job softness could snowball.

For housing, the balance matters. A controlled slowdown keeps borrowing costs stable—and stability, not euphoria, is exactly what NYC real estate needs heading into 2026.

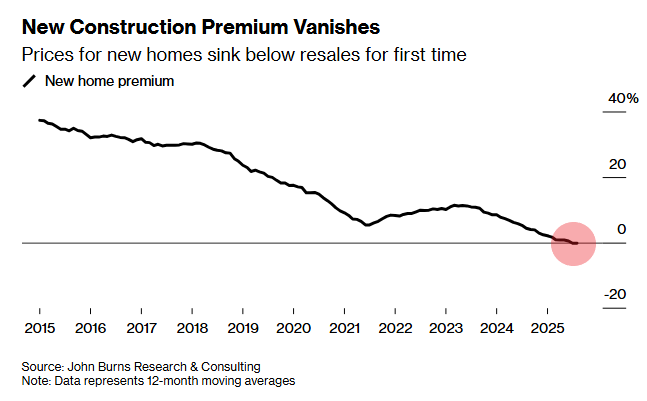

National Housing Snapshot: Builders Blink First

Across the country, the picture looks softer. New construction is under pressure, with builder premiums nearly gone. For the first time in years, resale homes are catching up—or even outperforming—new builds in price.

Developers are leaning on incentives—rate buy-downs, closing credits, free upgrades—to move inventory. But in Manhattan, where new development remains limited and expensive, the resale market continues to hold value.

The national slump underscores NYC’s unique position: it didn’t spike, so it doesn’t have to crash.

https://x.com/Barchart/status/1986592003849617483

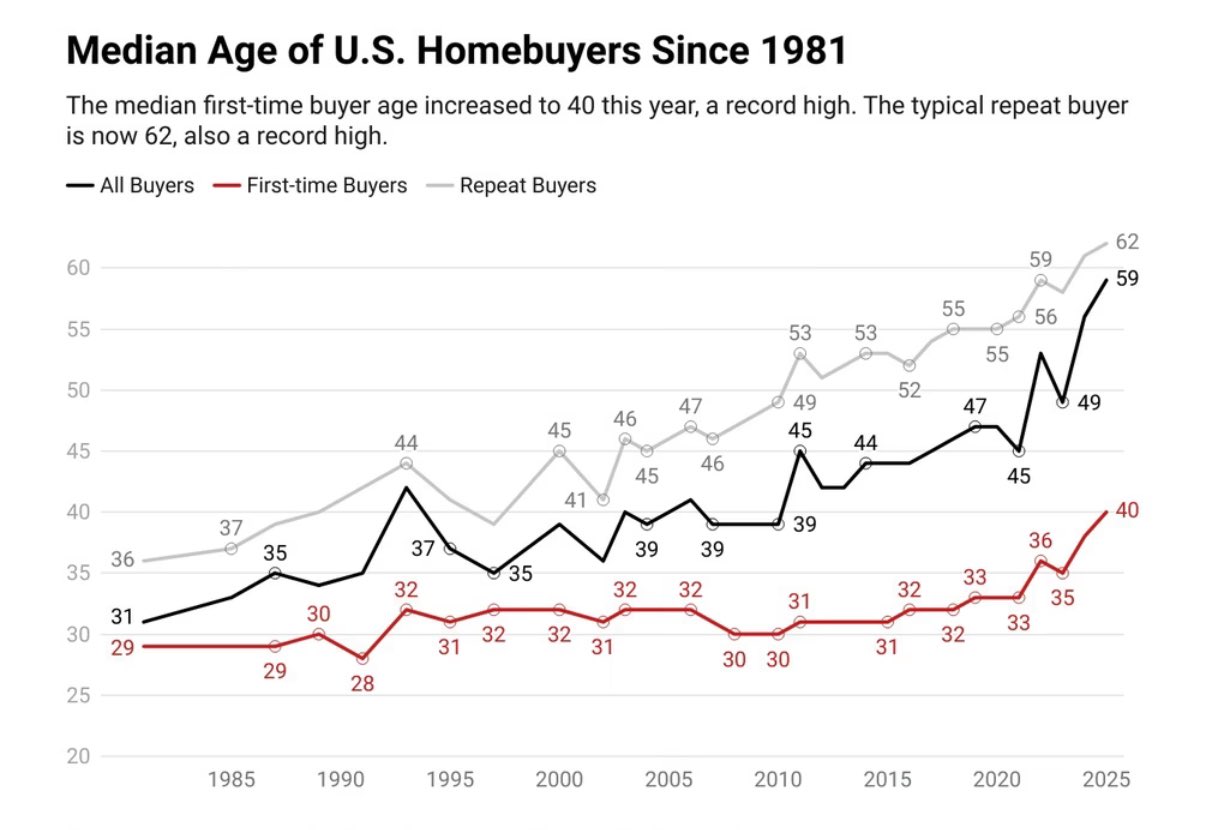

The Aging Buyer Base: A Structural Shift

Here’s a stat worth repeating. The median age of a U.S. homebuyer is now 59, up from 39 in 2005. For first-time buyers, it’s 40. For repeat buyers, it’s 62.

That’s a massive demographic shift—and it matters. Older buyers tend to move less frequently, stay longer, and hold more equity. Combine that with 71% of U.S. mortgages locked below 5%, and you get a recipe for a frozen housing cycle.

In Manhattan, this means fewer listings, longer hold times, and increasing rental demand. For investors and landlords, it’s a quiet tailwind. For buyers, it’s a reason to act sooner rather than later—because fresh inventory isn’t coming fast.

https://x.com/bobbyfijan/status/1986817366081093769

The Psychology Gap: Renovation Reality Check

One of the liveliest points in this week’s discussion came from the “renovation gap.” Sellers often value their decade-old upgrades as if they were done yesterday. Buyers? They see dated finishes and future costs.

That disconnect is one of the biggest friction points in today’s market. Condition is currency. Well-staged, freshly updated homes sell faster and closer to ask; dated ones get penalized heavily.

Staging, lighting, and subtle modern touches aren’t fluff—they’re leverage.

The Takeaway: A Market Defined by Quiet Strength

Manhattan’s late-2025 market doesn’t fit neatly into the boom-or-bust narrative. Supply is light, contracts are stable, and credit conditions are calm. Buyers are cautious but present; sellers are realistic but not desperate.

If 2024 was the year of frustration, 2025 is shaping up to be the year of clarity—a market returning to fundamentals, guided less by headlines and more by math.

Whether you’re a buyer watching rates, a seller eyeing timing, or simply trying to read the data between the headlines, this moment rewards strategy over speculation.

Let’s talk about where you fit into this November market—how to price smart, time your move, or seize an opportunity while others hesitate.

📩 Reach out today, and let’s map your next step with clarity and confidence.