What if the real estate market’s next move isn’t about prices—or even interest rates—but about something almost no one’s watching?

Reading the Room: Supply and Demand Are Both Cooling—But Not Equally

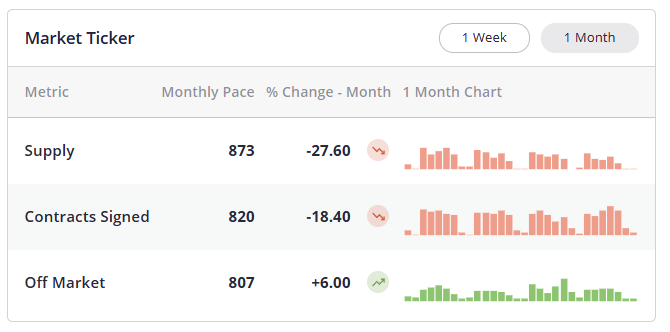

From July 12 to August 10, new listings in Manhattan totaled 873—well below the August average of 943. That’s not just a seasonal slowdown; it’s a lighter-than-usual supply drop. Contract signings also came in below trend, but not as steeply. In market terms, that means the pulse—the balance of leverage between buyers and sellers—is getting a slight upward push from the supply side.

It’s worth noting: contract signings saw a small bump in the last week of the period. That’s not enough to call it a rally, but it hints at some buyer resilience even as summer distractions pull people away from open houses.

The Macro Lens: Credit Spreads and Why They Matter for Real Estate

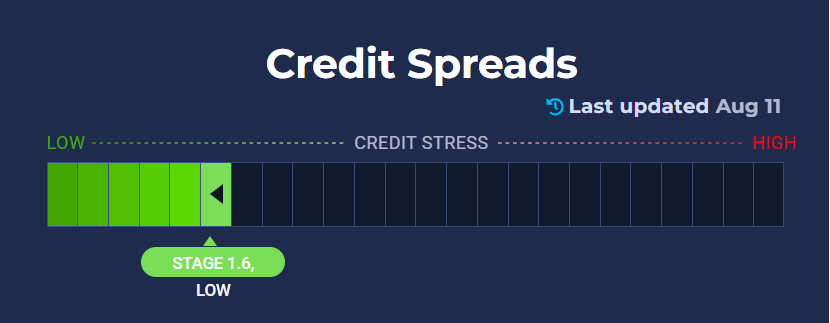

Credit spreads—the difference in yields between risky corporate bonds and safe government bonds—are like Wall Street’s mood ring. Narrow spreads signal calm, “risk-on” behavior; widening spreads indicate stress. Right now? They’re barely moving.

Why should a Manhattan buyer care? Because widening spreads tend to cool investment appetite across the board—stocks, bonds, and yes, real estate. Narrowing spreads can have the opposite effect. For now, the steady trend means no big warning signs, but also no fresh tailwinds.

https://www.creditspreadalert.com/

The Fed Factor: Rate Cuts Are Coming… But Don’t Expect a Mortgage Freefall

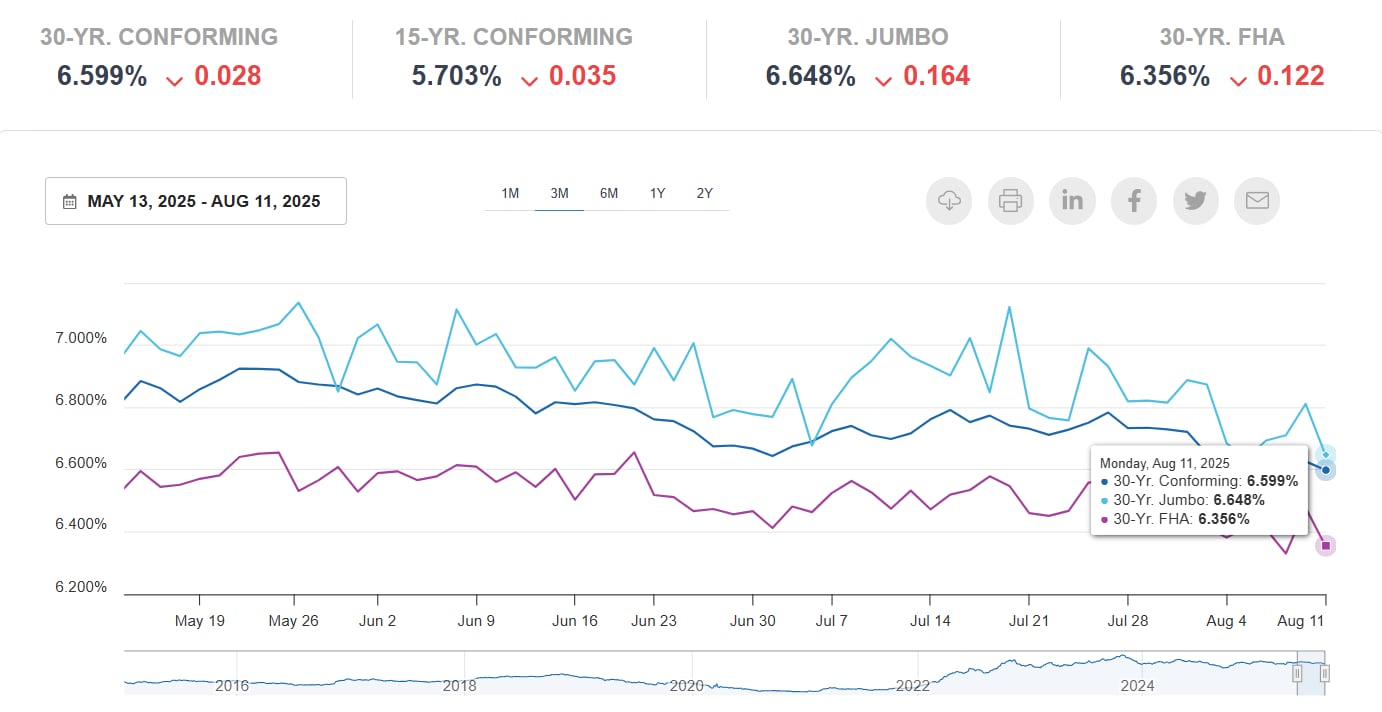

Markets are betting on an 86% chance of a quarter-point rate cut in September, with smaller odds of additional cuts in October and December. Here’s the catch: mortgage rates have likely priced that in already.

If you’re a buyer waiting for a major drop in your 30-year fixed rate the moment the Fed cuts? You might be disappointed. Mortgage rates tend to follow the 10-year Treasury yield more closely than the Fed Funds rate—and recent moves in the two-year and ten-year suggest only mild downward pressure ahead.

https://www2.optimalblue.com/obmmi

The Quiet Giant in CPI: Rent Trends Could Shift the Inflation Story

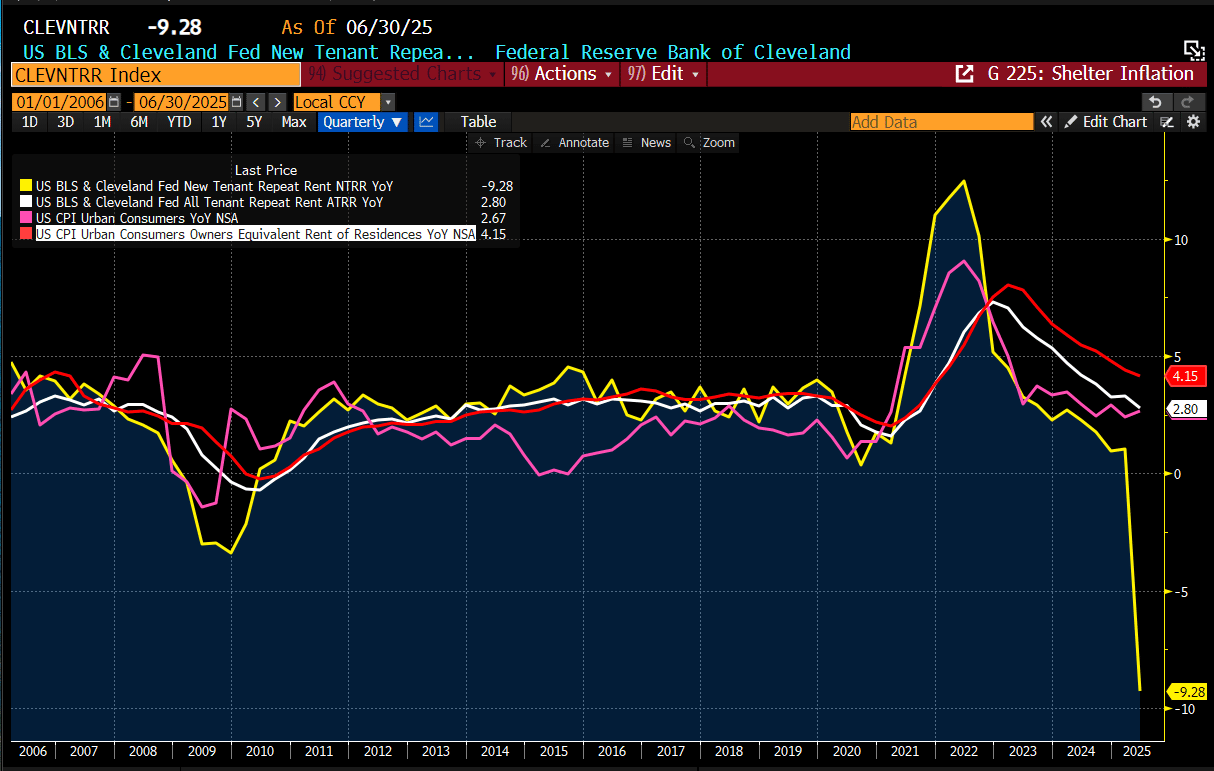

Here’s the surprising part: 25% of the Consumer Price Index is tied to “Owner’s Equivalent Rent,” a measure of housing costs. That measure usually follows broader rent trends with a lag. Right now, a key leading indicator—the “New Tenant Repeat Rent Index”—is plunging at its steepest pace in nearly two decades.

If that drop filters through as expected, it could lower the shelter component of CPI in the coming months. And lower inflation readings could give the Fed more room to cut rates in 2025—though tariffs and other price pressures may complicate the picture.

https://x.com/TheBondFreak/status/1953537652323455216

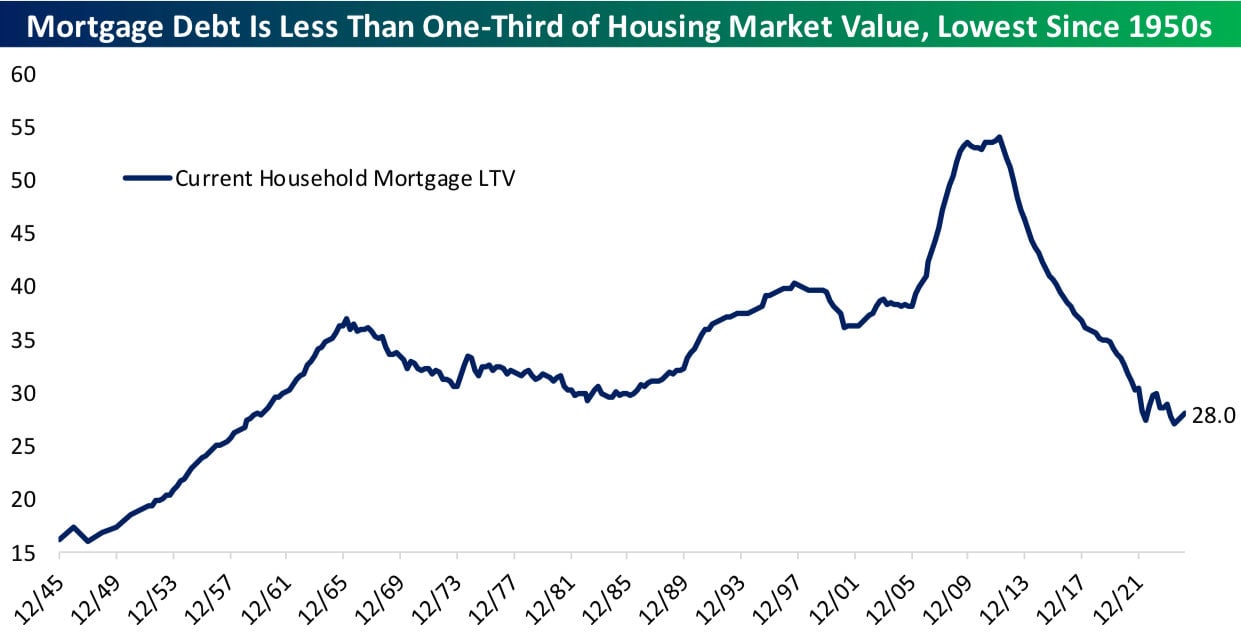

Why Manhattan Isn’t in a “Bubble” (Even if Other Markets Feel Frothy)

National headlines about “housing bubbles” miss a critical point: Manhattan hasn’t seen the same 100%+ price run-ups of some other regions over the past decade. Loan-to-value ratios are historically low, sellers are sitting on strong equity positions, and the structural risk is nothing like 2008.

In short, while national downturns can still cool local activity, the underlying health of NYC’s housing market is much stronger than the doom-and-gloom crowd might think.

https://x.com/bespokeinvest/status/1954541159726067817

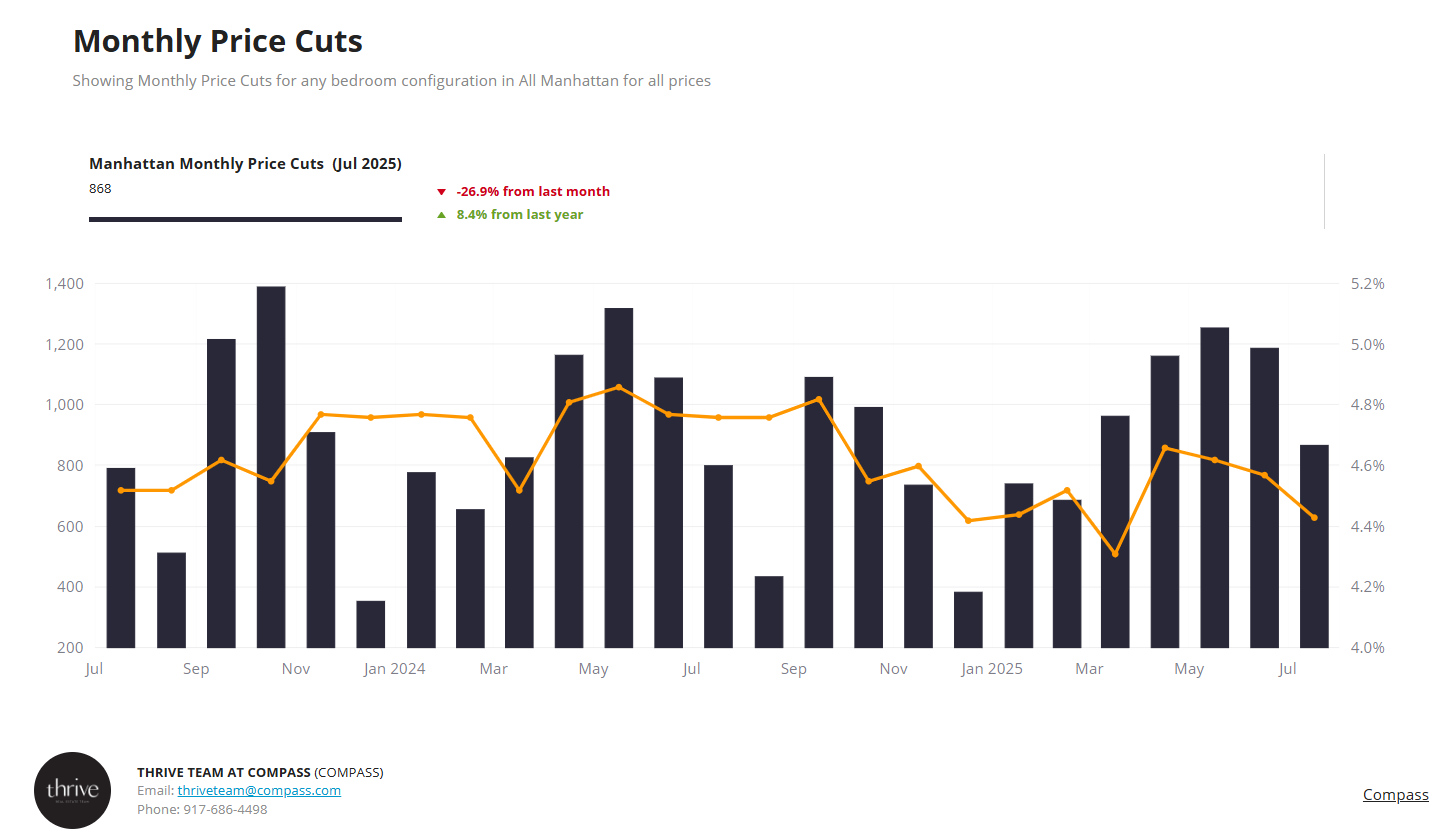

Strategy for Sellers: Timing and Price Cuts Matter More Than Ever

Plenty of agents are asking when to reduce prices on slow-moving listings. The data says the sweet spot is day 30 to day 60 within a high-activity season—spring or fall. Price cuts in off-season months, like mid-August, often fail to generate traction.

If you’re carrying a listing now, consider holding your next price adjustment until the early weeks of the fall market—when buyer activity traditionally rebounds. And if you’re advising sellers, use metrics like the Climate Index and sector-specific data to frame realistic expectations.

The Bottom Line for August 2025

- Inventory is below trend, giving sellers a bit of leverage.

- Demand is also below trend, so overpricing is still a risk.

- Rates may get modest relief from the Fed this fall, but don’t expect a sudden drop in mortgage costs.

- Rent trends could help cool inflation later this year, which might support more cuts in 2025.

- NYC remains structurally stronger than many national markets, even in a slowdown.

Final Thought: Local Matters Most

It’s easy to get lost in national headlines, but Manhattan buyers and sellers should remember: the real story is always local. Contract trends in your building, inventory in your neighborhood, and seasonal timing matter far more than macro buzzwords.

Thinking about making a move this fall?

Whether you’re eyeing a two-bedroom in Yorkville, a loft in Tribeca, or a townhouse in Brooklyn Heights, now’s the time to get your data lined up and your strategy sharp. Let’s talk through your goals, review the numbers that actually matter in your submarket, and set you up for success—before the market’s next turn.