January 2026 feels like that awkward pause between songs, when the beat hasn’t dropped yet, but you can tell the room is starting to wake up.

If you’ve been watching New York City real estate lately and thinking, “Something’s happening, but I can’t quite name it,” you’re not wrong. The market isn’t roaring. It isn’t frozen either. It’s hovering. Tight supply, hesitant buyers, steady rates drifting lower, and a lot of people waiting for someone else to make the first move.

This is the exact backdrop of Macro Monday, the weekly pulse check where Manhattan real estate meets the broader economy. And right now, that pulse tells a very specific story.

Let me explain.

The January paradox: Low energy, low inventory

January is never loud. It’s a reset month. But January 2026 is starting from an unusually low base.

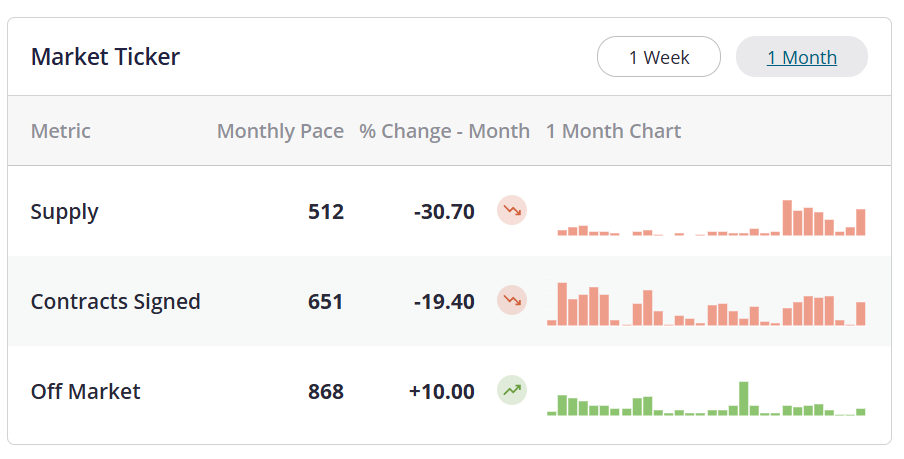

Manhattan inventory is sitting well below seasonal norms. We’re hovering around 512 active listings, when a typical January would expect closer to 1,300. That’s not a rounding error. That’s a structural shortage.

And yes, listings usually pick up later. April and September still rule as peak months. But starting this far behind matters. It shapes everything else, from pricing strategy to negotiation leverage.

Contract activity tells a similar story. Roughly 651 contracts signed over the last 30 days, compared to a seasonal expectation closer to 778. Historically, activity starts to lift around January 20th. We’re not there yet, but we’re getting close.

So no panic. Just patience.

A market that’s quiet, not broken

Here’s the thing people miss. December wasn’t actually bad. Contract volume came in slightly above expectations. It just didn’t last long. Holiday momentum faded fast.

Agents on the ground are reporting busy open houses. That’s not noise. That’s early pipeline activity. Traffic today often becomes contracts two or three weeks later. The data always lags real life.

This is why Mondays look soft. And why context matters.

Credit spreads aren’t blinking

If you want a real warning signal, you don’t start with listings. You start with credit.

Right now, credit spreads are flat and calm. No stress. No flashing red lights. That tells us the financial system isn’t worried. Investors are still comfortable taking risk. When credit spreads widen, everything changes. That’s not happening.

So while headlines might feel dramatic, the underlying machinery looks steady.

Risk is still on.

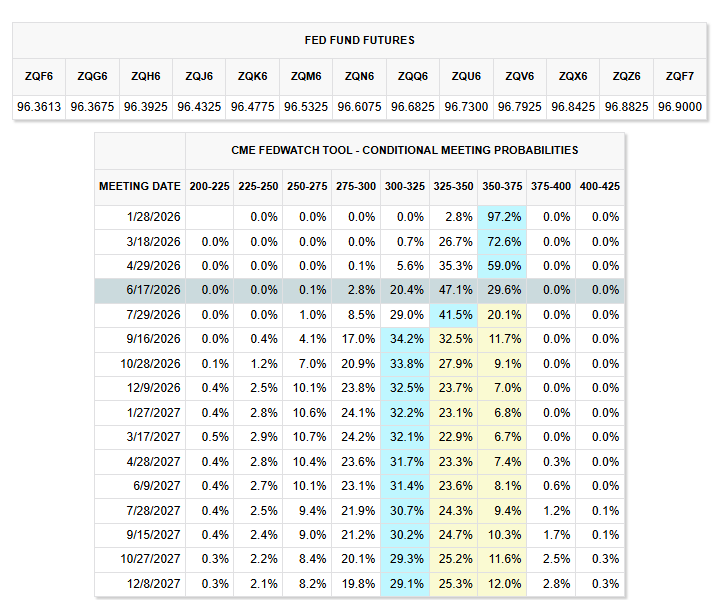

Interest rates: Fewer cuts, calmer moves

Markets are currently pricing in one possible rate cut around June 2026, with another maybe in October. Even June isn’t guaranteed. It’s close to a coin flip.

These aren’t emergency cuts. They’re normalization moves.

Mortgage rates, meanwhile, have quietly improved. Jumbo and conforming rates have drifted down from their 2023 peaks near 8 percent. We’re now seeing rates brushing the low 6 percent range again. Not cheap, but far more workable.

More important than the level is the behavior. The line is smooth. No violent jumps. That stability helps both buyers and sellers plan.

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Inflation isn’t gone, but it’s no longer screaming

Inflation is being stubborn, not explosive. Consumer expectations still hover above the Fed’s comfort zone. Job growth looks sluggish but not collapsing. That puts the Federal Reserve in an uncomfortable middle ground.

They can’t cut aggressively. They can’t hike either.

So we wait.

And markets adjust to that waiting.

Renovation fear is real, even when costs fall

Here’s a subtle but powerful force shaping NYC pricing right now. Perception.

Buyers still assume renovations cost three times what they used to. In some cases, that was true. In many cases, it no longer is. Materials have eased. Some labor costs have cooled. But expectations haven’t caught up.

So renovated units get rewarded. Anything needing work gets punished hard. Sometimes too hard.

That creates opportunity. If you can renovate efficiently, there’s real spread between fear-based pricing and reality.

Institutional investors aren’t the villain

You’ve probably heard the narrative. Big funds are buying all the homes. Prices are broken because of them.

The data says otherwise.

Institutional investors with large portfolios make up roughly 1 to 2 percent of the housing market. The rest is still owned by individuals and small operators. Mom-and-pop owners dominate.

Policy chatter around institutions may shift sentiment, but it won’t materially move NYC pricing. Still, perception shapes behavior, and behavior shapes markets.

Sellers: This is the hard truth

The listing climate remains challenging.

Many listings expired or went off-market in December, dragging the climate index down. That’s seasonal, but it’s also a warning. Aspirational pricing is not being rewarded right now.

A 2 percent price cut won’t spark urgency. Buyers need to feel value immediately. The first three weeks matter most. Miss that window, and momentum fades fast.

This is not a rising-tide market. It’s a lily-pad market. Correctly priced homes transact. Everything else waits.

Manhattan and Brooklyn: Similar mood, different texture

Manhattan showed a modest uptick into December. Brooklyn softened.

Luxury continues to behave better than sub-luxury. Rate sensitivity hits Brooklyn harder. Manhattan’s higher-end segments are more insulated.

Overall, both markets sit near the lower edge of neutral. Not collapsing. Not accelerating.

Stuck, but stable.

So what does all this actually mean?

Low supply is doing the heavy lifting right now, not surging demand. That gives sellers some leverage, but only if they’re realistic. Buyers have more patience than they did a few years ago, and they’re using it.

Rates are no longer the villain. Renovation fear still is. Seasonality is about to matter more by late February and March.

And this moment, quiet as it feels, is usually where smart positioning happens.

A natural next step

If you’re buying, selling, or advising clients in NYC right now, this is not the time for shortcuts or gut guesses. Market timing, pricing strategy, and seasonal awareness matter more than ever. If you want a clearer read on how these macro forces translate to your specific property or neighborhood, this is where informed guidance makes the difference. A thoughtful, data-backed strategy now can save months of frustration later. And in a market this selective, clarity is real leverage.