Are we in a slow summer slump—or standing on the edge of the next market move?

If you’ve been feeling like something’s off in the New York City real estate market lately, you’re not wrong. But let’s be honest—it’s not some massive crash or dramatic correction. It’s more like a long inhale. Everyone’s waiting. Sellers. Buyers. The Fed. You. Me. The entire market feels like it’s holding its breath.

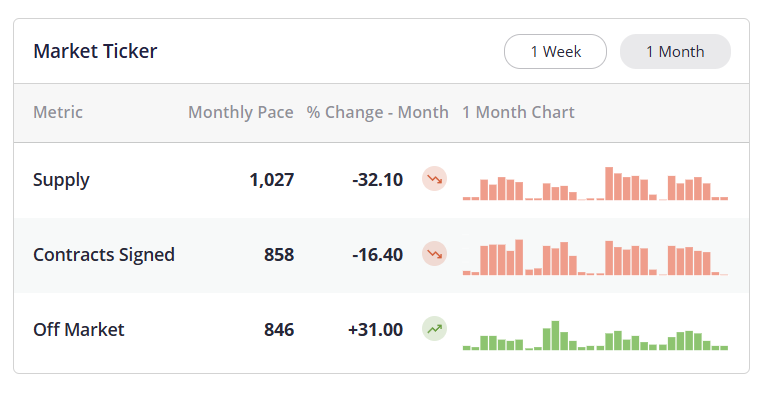

Inventory’s Down—And That’s the Real Story

Let’s start with what’s not happening: listings.

As of July 21, Manhattan had just 1,027 new listings over the past month—down about 13% from where we should be seasonally. That’s not just a number; that’s hundreds of would-be sales never entering the ring. Buyers aren’t being picky—they’re being left with slim pickings.

There’s no last-minute surge on the horizon either. Even the brokers are on vacation.

Contracts Are Holding Steady—But Don’t Be Fooled by the Pulse

With inventory slipping, you might expect contract activity to nosedive too. But it hasn’t. Over the past 30 days, Manhattan logged 858 contracts—about 6% below the seasonal average of 917. Not exactly booming, but not falling off a cliff either.

So what’s the takeaway? Buyers are still out there—they’re just taking their sweet time. No one’s in a frenzy. They’re browsing, not bidding wars. Waiting for prices to soften... or interest rates to blink first.

Now, if you’ve seen charts showing the market “pulse” trending upward, don’t get too excited. That doesn’t mean demand is heating up—it means supply is falling faster than contracts.

It’s not a resurgence. It’s a recalibration. The summer slowdown for sellers is making the market look deceptively stronger.

In reality? The music’s quieter because half the band is on vacation.

Rate Cuts? Maybe. Cheaper Borrowing? Don’t Count on It.

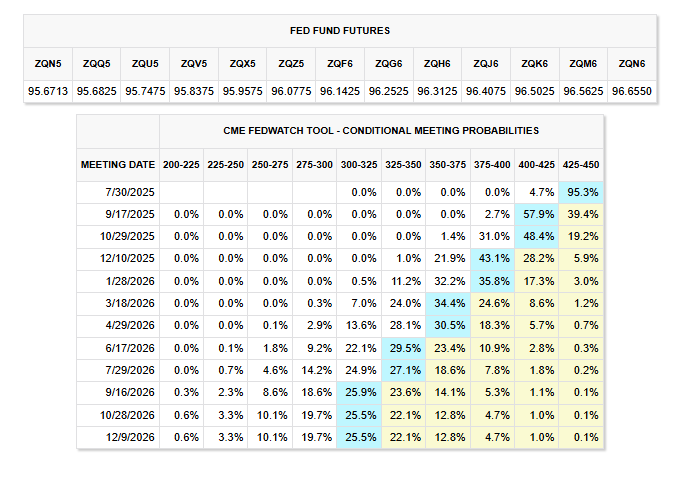

Everyone’s watching the Fed—and honestly, the Fed might be watching us just as nervously.

As of now, there’s a 95% chance rates will hold steady in July. September? That’s a toss-up. Markets are pricing in a 56% chance of a cut, but that number used to be in the high 60s. Confidence is slipping.

But here’s the kicker: the last time the Fed cut rates, mortgage rates actually went up. Why? Because this isn’t checkers—it’s chess. And the board’s missing a few pieces.

JP Morgan’s Oxana Aronov explained it best: the Fed controls the Fed funds rate, not your mortgage rate. Long-term borrowing costs react to a whole stew of factors—market sentiment, inflation expectations, political stability.

If confidence in the Fed's independence starts to wobble—say, amid election-year theatrics—long-term rates could rise even if Powell cuts.

Bottom line? A rate cut might not mean cheaper borrowing. The narrative matters as much as the numbers. Maybe more.

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

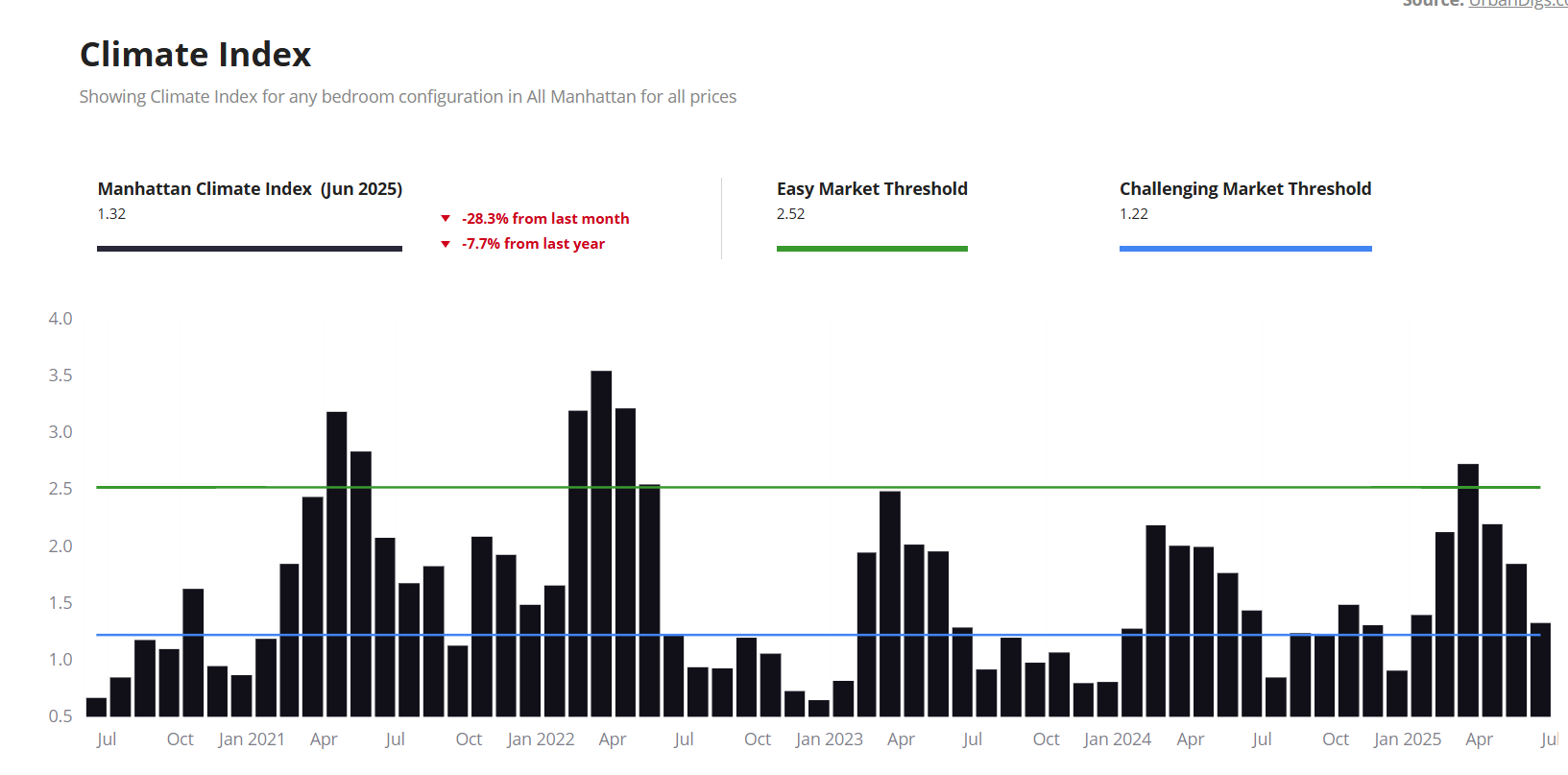

Tight Supply, Stalled Sellers, and a Quiet Foreign Comeback

Nationwide, new multi-family construction has been slowing since 2022, thanks to high borrowing costs. Fewer projects mean tighter supply—and buyers circling stale inventory.

In NYC, it’s more complicated. Average resale condo prices may look strong, but that masks a softer reality. Sellers who bought during the 2015–2017 peak—and didn’t renovate—are often breakeven or worse. Price cuts are common, especially below $4 million.

The Listing Climate Index backs that up. We’re firmly in “challenging” territory—nothing like the hot streak of 2014–2015. So while price-per-foot may say one thing, the lived experience says another.

One bright spot? Foreign buyers. With the U.S. dollar down in 2025, European buyers are effectively getting 10–15% discounts. If you’ve got an international client who’s been waiting for a reason... this might be it.

Bottom Line: It’s Not Broken. It’s Just... Sideways

The Manhattan market isn’t crashing. It’s recalibrating. There’s no panic. But there’s no rush, either. Sellers are hesitant, buyers are cautious, and everyone is watching rates like hawks. In this kind of market, nuance matters more than ever.

Thinking of selling or buying in this sideways moment? Let’s chat. Whether you’re weighing the value of a 2016 purchase, considering a currency advantage, or just unsure where your property stands, we’ll unpack the data together—no pressure, just perspective.