Seasonal slump, foreign buying power, and an eye on September: Here’s what’s really happening behind the numbers.

Is the Manhattan real estate market quietly shifting beneath our feet—and are international investors the only ones noticing?

Midtown Malaise: July’s Market Check-In

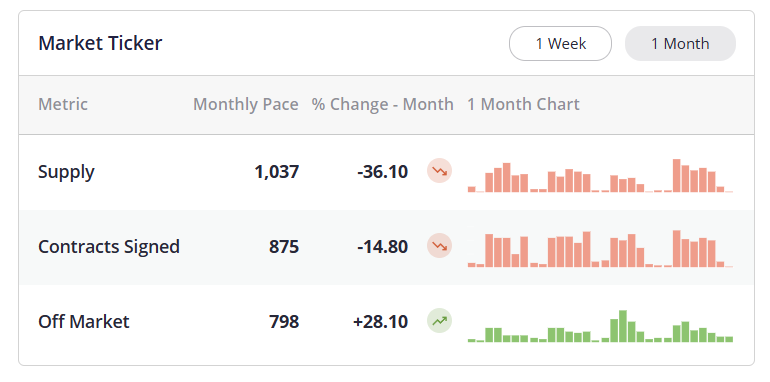

It’s summer in New York, and real estate is doing what it usually does—slowing down. But this time, the cooldown feels... quieter. According to UrbanDigs’ July 14 Macro Monday update, both supply and contract activity in Manhattan are trending below historical averages.

By mid-July, new listings were already lagging the monthly norm (1171), and contract activity was pacing 5% under its seasonal benchmark. The punchline? Liquidity—which had spent the first half of 2025 up year-over-year—has now turned negative.

Still, don’t sound the alarm. This isn’t a collapse—it’s a seasonal sag, made more dramatic because supply is falling faster than demand. That’s creating a market pulse illusion: it looks like strength on paper, but it’s really just the result of fewer homes being listed.

Credit Spreads: Just a Hiccup, or Something More?

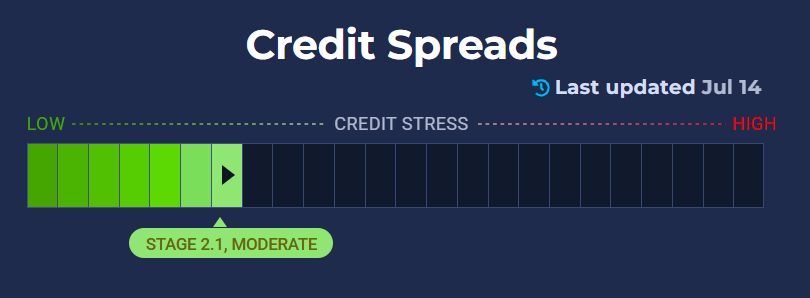

UrbanDigs tracks a proprietary Credit Spread Indicator—basically, a stress gauge for the global credit system. On July 14, that gauge ticked up from 1.6 to 2.1 (out of a 4-stage system). It’s a small move, but one that deserves a side-eye.

Why? Because credit stress tends to precede risk-off behavior—stocks retreat, bond yields shift, and fear creeps in. While this current move isn’t dramatic, it suggests investors are starting to notice headline risks again, particularly around global tariffs and trade tensions.

The key takeaway: we're not in panic mode, but we’re also not cruising carefree. If spreads tick up again—to 2.3 or 2.4—you’ll start to see the broader market react.

https://www.creditspreadalert.com/

Will the Fed Actually Cut? Don’t Bet the House Just Yet

The Fed funds rate currently sits between 4.25% and 4.5%, and CME FedWatch futures show a 95% chance of no movement at the July 30 meeting.

But come September? The market's baking in a 61% chance of a rate cut—and a 43% chance of another in December. That said, the Fed’s tone will matter more than the cut itself.

Here’s the thing: a single rate cut won’t move the mortgage needle much if the Fed signals it’s one and done. Conversely, a dovish message could shift expectations even if the actual cut is modest. Markets move on what’s next, not what’s now.

And while inflation has cooled (trueflation.com suggests 1.7% annually), the Fed’s still playing a data-waiting game. A cut’s possible... but far from guaranteed.

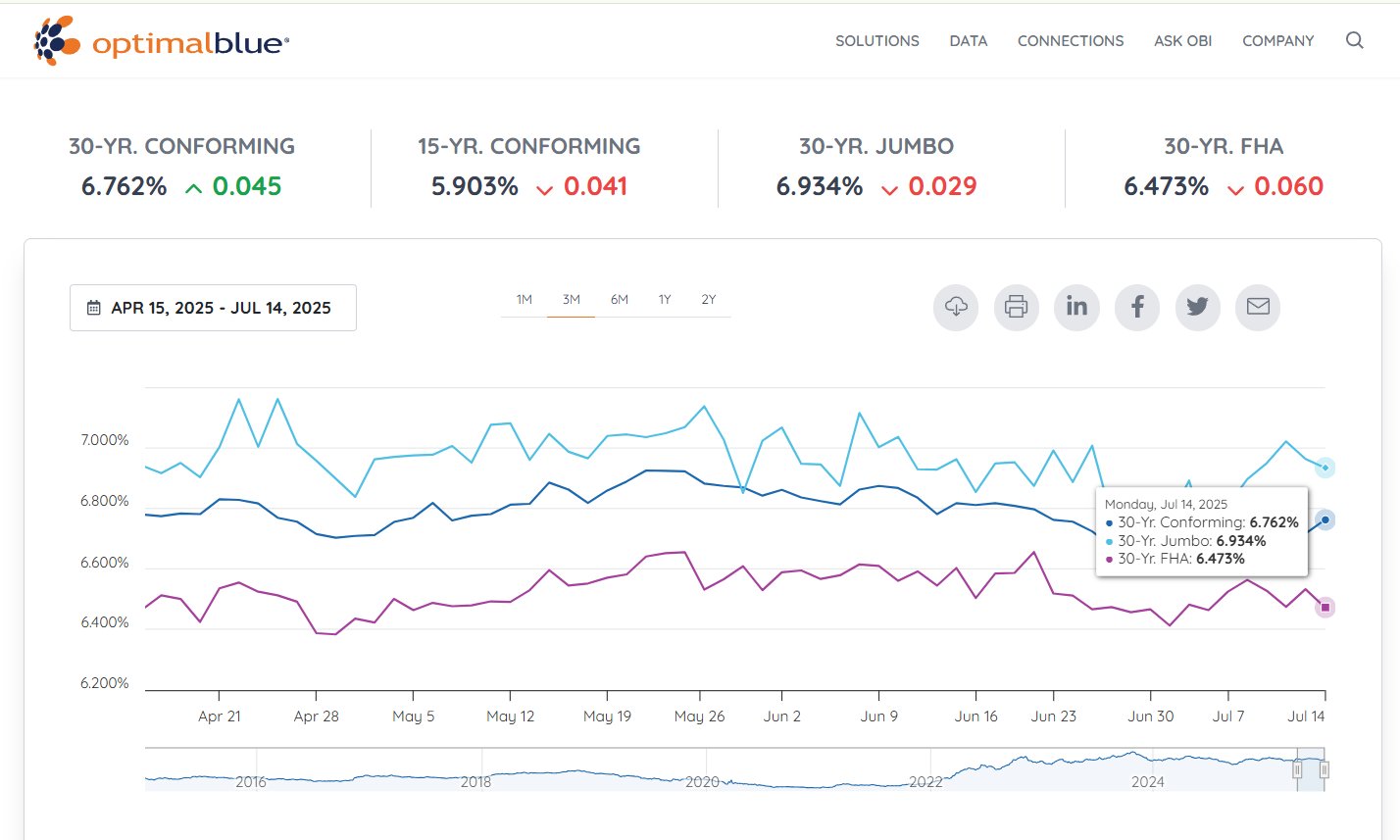

Mortgage Rates: Floating in the High Sixes

Average 30-year fixed mortgage rates are hovering around 6.77%—and they’ve been stuck in this upper-6% band for months.

We’re nowhere near the brutal double-digits of the 80s, but let’s not kid ourselves: it’s a rude awakening for anyone who refinanced at 2.75% three years ago. That sharp shift is freezing many sub-$2M buyers, especially in Manhattan and Brooklyn.

Luxury buyers, meanwhile, keep buying. Rates don’t scare someone dropping $5M+. But for entry and mid-level purchasers, today’s rates mean real affordability strain.

https://www2.optimalblue.com/obmmi

Foreign Buyers, Take Note: Manhattan Is on Sale

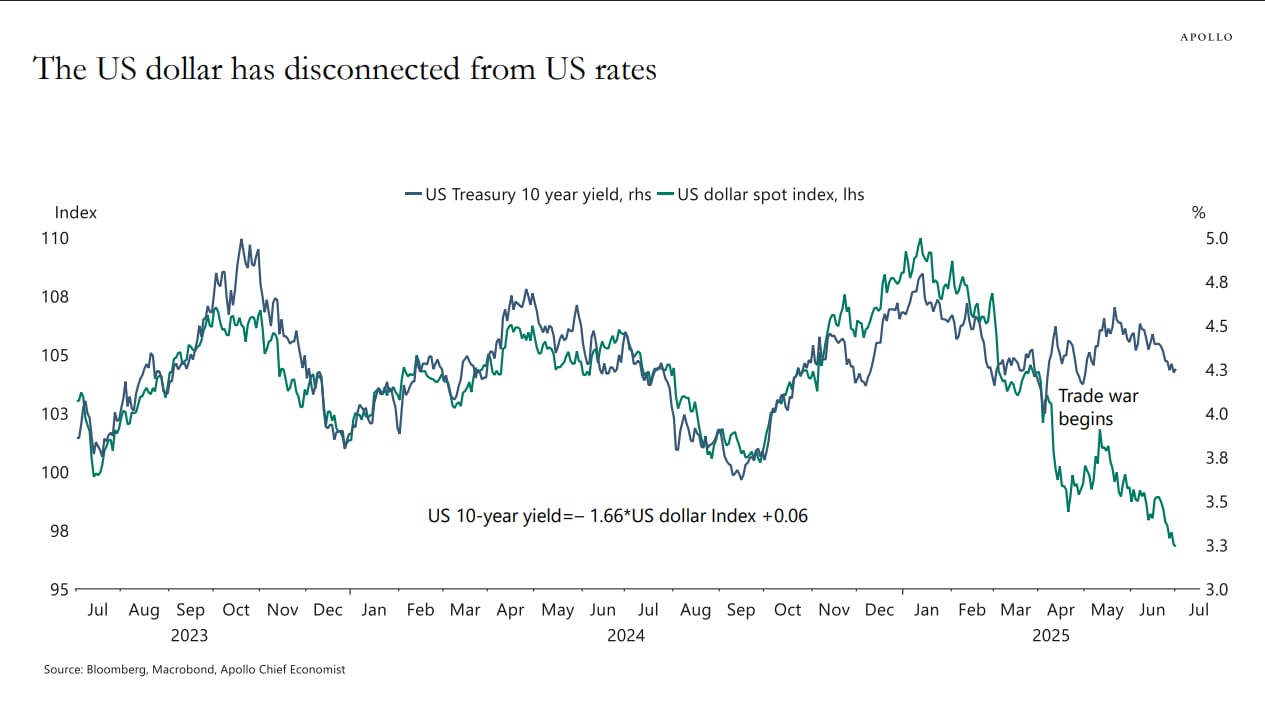

Here’s the curveball: while NYC prices appear stable in dollars, they’re falling in euros. Thanks to a weakening U.S. dollar, foreign buyers—especially in Europe—are seeing 10–15% discounts simply on currency conversion.

So if you're holding euros, pounds, or crowns, a resale condo in Manhattan might now look like a relative bargain.

That’s especially true if rents continue their upward trend and the dollar regains value after purchase. Add in even modest appreciation and foreign buyers could enjoy a nice tailwind—without needing a home run.

What’s holding them back? Likely political policy risk, regulatory shifts, and lingering caution from international investors burned during NYC’s pandemic-era whiplash.

https://www.apolloacademy.com/wp-content/uploads/2025/07/Outlook2025H2-071325.pdf

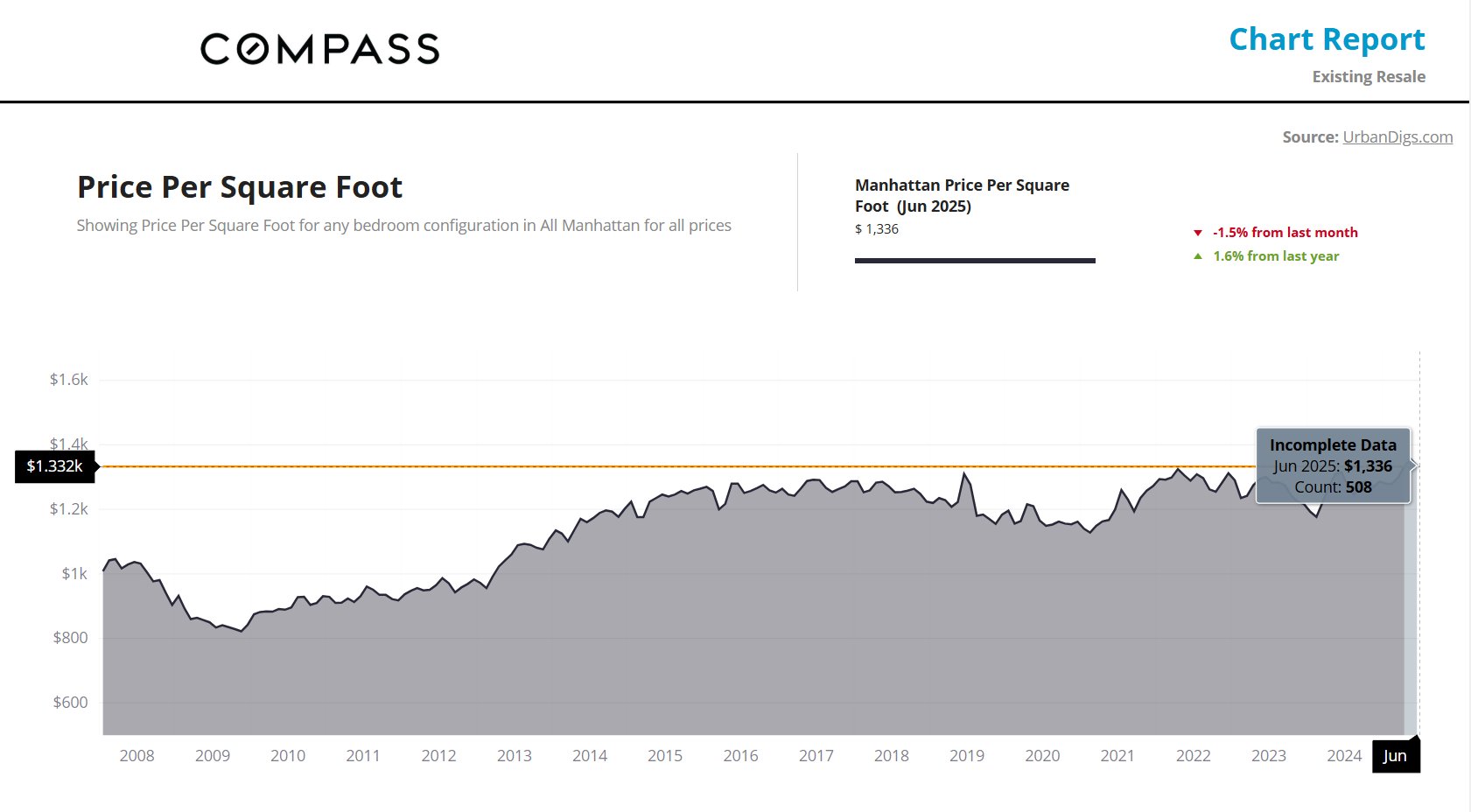

Prices vs. “The Vibe”: A Growing Disconnect

One of the most compelling charts shared during Macro Monday was the divergence between price action and market “climate.”

Price per square foot for resale condos has been relatively flat for over a year. But UrbanDigs’ climate index—a sentiment-driven measure of listing strength—has dipped to near-challenging levels.

Translation: Sellers see stable prices, but buyers (and agents) are feeling soft ground beneath their feet.

That divergence explains why so many deals are stalling post-showing: expectations are misaligned. Unless September brings a buyer resurgence, pricing could face more pressure.

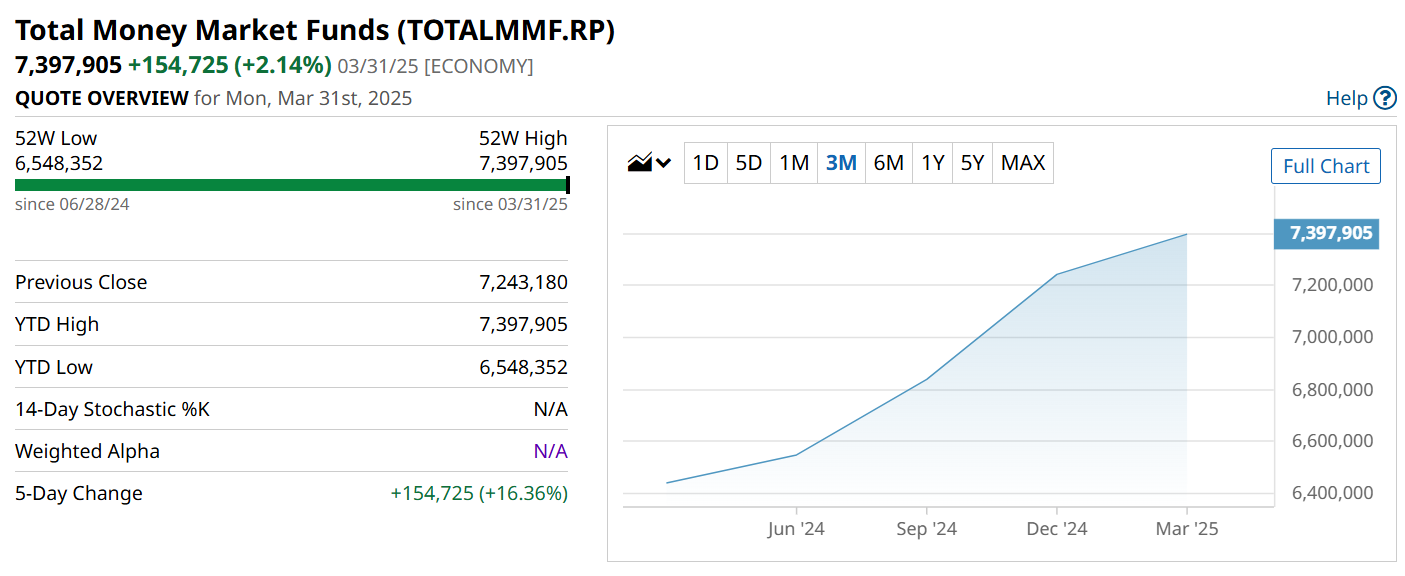

On the Sidelines: $7.4 Trillion in Cash

Yes, trillion with a “T.” That’s the amount sitting in money market funds as of this month.

Blame it on 4.5% yields and investor exhaustion. When you can park your money risk-free and earn decent returns, jumping into an overheated stock market—or a tepid housing market—just isn’t that appealing.

This wall of cash might eventually fuel asset rallies. But for now, it’s a barometer of buyer hesitation, especially among high-net-worth individuals who would normally be shopping luxury properties this summer.

https://www.barchart.com/stocks/quotes/TOTALMMF.RP

AI, Crypto, and Consumer Strength

A few digressions from Macro Monday worth noting:

-

Bitcoin has surged past $123,000, and other assets not priced in dollars (like gold) are rising alongside it.

-

AI is impacting employment, especially among recent grads, and may be a factor in rising inequality concerns.

-

Credit card delinquencies, surprisingly, are declining—even among younger borrowers. That’s a big signal the consumer remains strong, which might explain the Fed’s hesitation to cut rates just yet.

So, What Happens This Fall?

The summer market is sleepy, as expected. But what matters now is what happens in September and October. Will buyers return, refreshed and ready to deal? Will rates hold—or spike again? Will currency trends spur more foreign sales?

And maybe the big wildcard: will NYC’s political winds scare off investment, or simply blow more opportunity toward the savvy and prepared?